Thomas Rowe Price Jr. fundamentally changed Wall Street in the 1930s by looking past depressed, undervalued assets to find companies capable of long-term earnings expansion. He codified the principles of growth investing, shifting the industry focus toward future earning power, management quality, and economic cycles. This collection breaks down his philosophy on finding "fertile fields," navigating the corporate life cycle, and aligning investment fees with client success.

Part 1: The Core Philosophy of Growth

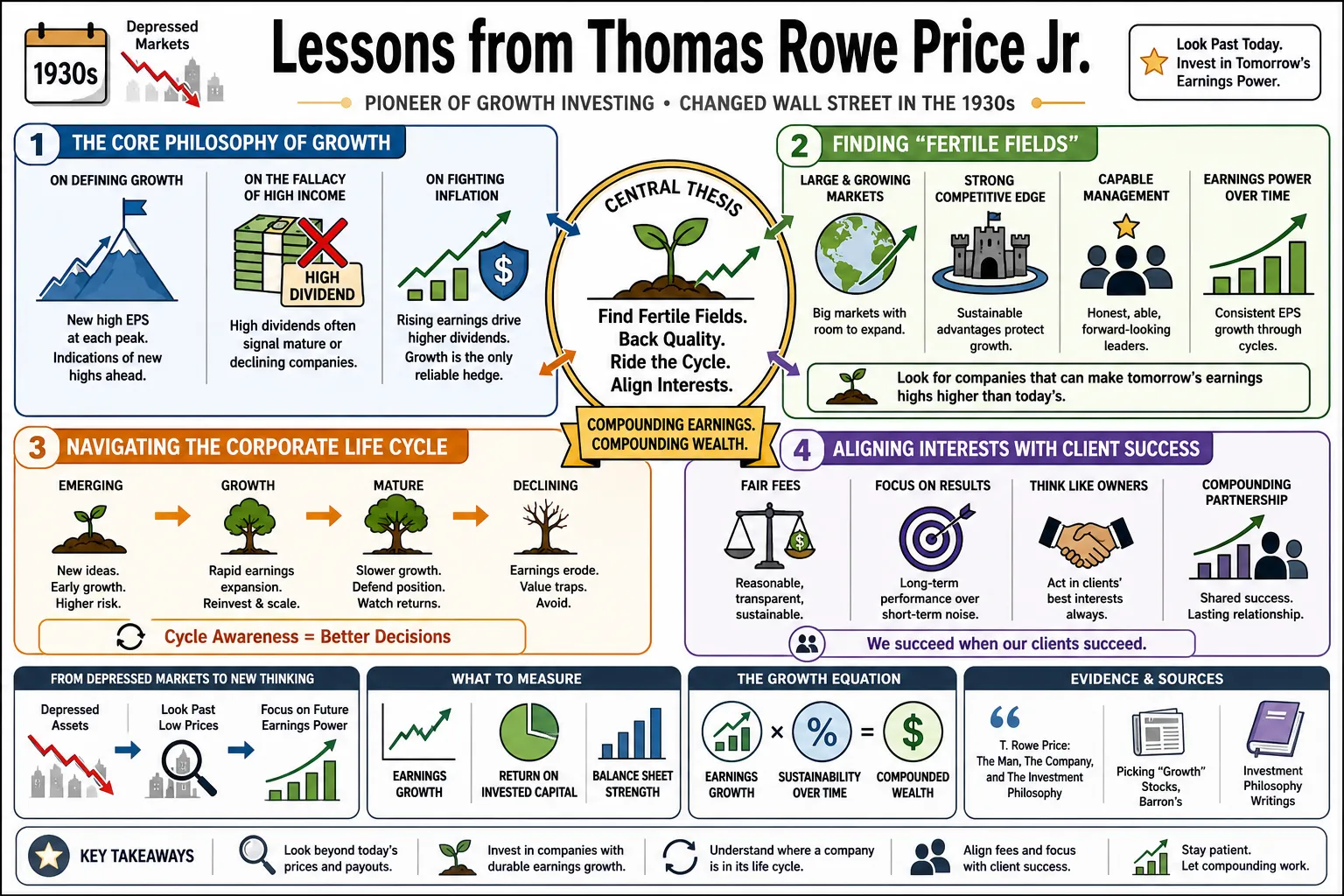

- On defining growth: "A growth company is one whose earnings per share reaches a new high level at the peak of each succeeding major business cycle and gives indications of reaching new high earnings at the peak of future business cycles." — Source: T. Rowe Price: The Man, The Company, and The Investment Philosophy

- On the fallacy of high income: Seeking high current dividends often leads investors into mature or declining companies rather than those capable of compounding wealth. — Source: Picking "Growth" Stocks, Barron's

- On fighting inflation: Growth stocks are the only reliable way to outrun the erosion of inflation, as rising earnings eventually dictate higher dividends and capital appreciation. — Source: Picking "Growth" Stocks, Barron's

- On compounding wealth: "Most big fortunes result from investing in a growing business and staying with it through thick and thin." — Source: The Money Masters

- On simplicity: "To find a fertile field to invest in you didn't have to go to college, you only needed what my grandmother called horse sense." — Source: T. Rowe Price: The Man, The Company, and The Investment Philosophy

- On predictive limits: "No one can see ahead three years, let alone five or ten. Competition, new inventions—all kinds of things—can change the situation in twelve months." — Source: T. Rowe Price: The Man, The Company, and The Investment Philosophy

- On market formulas: "No mathematical formula or yardstick alone can be relied on for identifying growth stocks or for detecting when their earnings reach maturity." — Source: The Money Masters

- On basic observation: "If you stay half-alert, you can pick the spectacular performers right from your place of business or out of the neighborhood shopping mall, and long before Wall Street discovers them." — Source: T. Rowe Price: The Man, The Company, and The Investment Philosophy

- On early adoption: The best time to invest in a business is when it is small, before its shares gain wide stature and sell at high price-to-earnings ratios. — Source: The Money Masters

- On top-down and bottom-up analysis: Successful investing requires identifying the right industries first, then doing the fundamental research to find the best-managed companies within them. — Source: The Money Masters

Part 2: The Corporate Life Cycle

- On biological parallels: "Earnings of most corporations pass through a life cycle which, like the human cycle, has three important phases — growth, maturity, and decadence." — Source: The Money Masters

- On maximum gain: The greatest possibility for capital gain, accompanied by the least risk, occurs when the long-term earnings trend of a young company is highly positive. — Source: The Money Masters

- On the maturity phase: When a company’s rate of return on invested capital levels off, it ceases to be a true growth stock and becomes overly sensitive to the general economic cycle. — Source: Picking "Growth" Stocks, Barron's

- On the decadence phase: A corporation in decline loses its competitive edge, suffers stagnant earnings, and falls victim to obsolescence or poor management. — Source: Picking "Growth" Stocks, Barron's

- On the rule for aging companies: Investors should sell immediately once it becomes obvious a company has entered its decadence phase. — Source: The Money Masters

- On assessing risk by age: Just as insurance companies know it is riskier to insure a 50-year-old than a 25-year-old, investors must recognize the inherent risks in aging corporations. — Source: T. Rowe Price: The Man, The Company, and The Investment Philosophy

- On crowded fields: Maturity in a business cycle is often signaled when a once-fertile field becomes saturated with competitors. — Source: Picking "Growth" Stocks, Barron's

- On index stagnation: Avoiding the mature companies that historically weighed down the Dow Jones Industrial Average is as critical as picking the winners. — Source: T. Rowe Price: The Man, The Company, and The Investment Philosophy

- On shifting focus: The investor's primary job is to track where a company sits in its life cycle, moving capital away from maturity and toward emerging growth. — Source: The Money Masters

- On timing the exit: "The trick is to buy in the growth phase and sell before the decline begins." — Source: The Money Masters

Part 3: The Certainty of Change

- On market absolutes: "Change is the investor's only certainty." — Source: T. Rowe Price: The Man, The Company, and The Investment Philosophy

- On recognizing eras: "It is better to be early than too late in recognizing the passing of one era, the waning of old investment favorites and the advent of a new era affording new opportunities for the investor." — Source: T. Rowe Price: The Man, The Company, and The Investment Philosophy

- On industry lifespans: Because industries inevitably mature and decline, investors must constantly research new sectors to replace dying ones. — Source: The Money Masters

- On market panic: During the onset of World War II, Price advised clients that this was no time to be panicky, urging them to ignore rumors and focus on structural long-term growth. — Source: T. Rowe Price: The Man, The Company, and The Investment Philosophy

- On proactive behavior: "The man who waits for some seventh wave to toss him on dry land will find that the seventh wave is a long time a-coming." — Source: T. Rowe Price: The Man, The Company, and The Investment Philosophy

- On the folly of waiting: "You can commit no greater folly than to sit by the roadside until someone comes along and invites you to ride with him to wealth or influence." — Source: T. Rowe Price: The Man, The Company, and The Investment Philosophy

- On intellectual flexibility: The capacity to abandon long-held theories when the macroeconomic environment shifts is a requirement for survival. — Source: T. Rowe Price Associates History

- On continuous research: The fact that no one can predict the next decade means research cannot be a periodic event; it must be a continuous process of observation. — Source: The Money Masters

- On ignoring the crowd: Price operated outside the Wall Street establishment in Baltimore, purposefully distancing himself from the groupthink of financial centers. — Source: T. Rowe Price: The Man, The Company, and The Investment Philosophy

- On adapting to conditions: A strategy must fit the times. When pure growth investing stopped working in the late 1960s, Price built a completely different framework to handle inflation. — Source: T. Rowe Price: The Man, The Company, and The Investment Philosophy

Part 4: Identifying the "Fertile Field"

- On selecting industries: Investors should identify industries in their early stages of development—fertile fields—and then buy the leading companies within them. — Source: The Money Masters

- On competitive moats: A fertile field is characterized by a distinct lack of cut-throat competition, allowing companies to maintain pricing power. — Source: Picking "Growth" Stocks, Barron's

- On regulatory immunity: Price preferred companies that operated with comparative freedom from government interference, wage controls, and rate regulation. — Source: Picking "Growth" Stocks, Barron's

- On labor costs: Ideal growth companies have low total labor costs as a percentage of sales but still pay their employees well enough to ensure high productivity. — Source: Picking "Growth" Stocks, Barron's

- On research and development: Intelligent R&D that develops new products and markets is essential if a company is to forge ahead in a rapidly changing world. — Source: Picking "Growth" Stocks, Barron's

- On capital requirements: A company must have finances strong enough to weather periods of adverse earnings without facing insolvency. — Source: Picking "Growth" Stocks, Barron's

- On return on capital: A growth stock must sustain a reasonable return on invested capital, historically defined by Price as 8 percent or above. — Source: Picking "Growth" Stocks, Barron's

- On efficiency: The ability to lower production costs and expand into new markets without reducing the return on invested capital is a hallmark of a fertile field. — Source: The Money Masters

- On sustained margins: Profit margins must remain reasonable relative to the industry average over multiple economic cycles. — Source: The Money Masters

Part 5: Assessing Quality and Management

- On the human element: "Every business is manmade. It is a result of individuals. It reflects the personalities and the business philosophy of the founders and those who have directed its affairs throughout its existence." — Source: T. Rowe Price: The Man, The Company, and The Investment Philosophy

- On understanding a business: "If you want to have an understanding of any business, it is important to know the background of the people who started it and directed its past and the hopes and ambitions of those who are planning its future." — Source: T. Rowe Price: The Man, The Company, and The Investment Philosophy

- On management vision: "The growth of a company is the result of the vision and ability of its management." — Source: The Money Masters

- On executive ownership: Directors and officers should hold substantial stock in their companies to ensure their interests align with shareholders. — Source: Picking "Growth" Stocks, Barron's

- On executive compensation: Management motives should be driven by equity appreciation, not overshadowed by excessive salaries and bloated pensions. — Source: Picking "Growth" Stocks, Barron's

- On employee goodwill: Aggressive and efficient leadership means little if it does not actively cultivate and maintain the goodwill of its workforce. — Source: Picking "Growth" Stocks, Barron's

- On social awareness: Leadership must understand underlying social trends to navigate long-term shifts in consumer behavior and regulation. — Source: Picking "Growth" Stocks, Barron's

- On dividend growth: A company's ability to consistently raise its dividend is the ultimate proof of genuine earnings power and management discipline. — Source: The Money Masters

- On reading broadly: Price required his analysts to consume the news daily; a failure to read the morning financial papers was considered a dereliction of duty. — Source: T. Rowe Price: The Man, The Company, and The Investment Philosophy

Part 6: Inflation and the "New Era"

- On recognizing the end of growth: By the late 1960s, Price observed that the post-WWII period of stable industrial growth was ending, prompting a radical shift in his framework. — Source: T. Rowe Price Associates History

- On currency devaluation: "People will not want paper dollars. They will want tangible property: land, natural resources, timber, minerals in the ground." — Source: T. Rowe Price: The Man, The Company, and The Investment Philosophy

- On hard assets: The New Era philosophy directed capital toward companies that owned physical resources, providing intrinsic value that rises alongside inflation. — Source: T. Rowe Price Associates History

- On resource scarcity: Price anticipated that essential natural resources would become increasingly scarce, driving their value higher independent of broader market trends. — Source: The Money Masters

- On adapting the growth model: The New Era Fund demonstrated that traditional growth strategies could be successfully adapted to include inflation-sensitive assets. — Source: T. Rowe Price: The Man, The Company, and The Investment Philosophy

- On protecting purchasing power: The ultimate goal of investing during high inflation is not capital appreciation, but the defense of raw purchasing power. — Source: T. Rowe Price Associates History

- On identifying inflation survivors: Price targeted companies that could remain profitable even as their labor costs and input prices rose dramatically. — Source: T. Rowe Price: The Man, The Company, and The Investment Philosophy

- On gold and silver: During the stagflation of the 1970s, Price moved heavily into precious metals to hedge against the declining value of the U.S. dollar. — Source: T. Rowe Price Associates History

- On ignoring early underperformance: The New Era strategy struggled initially before surging nearly 130 percent between 1978 and 1981, validating his willingness to be early. — Source: T. Rowe Price: The Man, The Company, and The Investment Philosophy

Part 7: Discipline, Patience, and Risk

- On the mental toll of trading: "The growth stock theory of investing requires patience, but is less stressful than trading, generally has less risk, and reduces brokerage commissions and income taxes." — Source: The Money Masters

- On broad diversification: "When picking a list of growth stocks for long-term investment, broad diversification of the risk is the first and most important principle to follow." — Source: T. Rowe Price: The Man, The Company, and The Investment Philosophy

- On the impossibility of perfect foresight: Because no one can look five or ten years ahead and guarantee the best single stock, spreading risk across multiple fertile fields is mandatory. — Source: T. Rowe Price: The Man, The Company, and The Investment Philosophy

- On the 25/75 rule: Price estimated that even with rigorous research, an investor might only be right about a true long-term growth stock 25 percent of the time. — Source: Picking "Growth" Stocks, Barron's

- On asymmetrical returns: The massive gains generated from the 25 percent of winning stock picks will more than cover the losses from the 75 percent that fail to meet expectations. — Source: Picking "Growth" Stocks, Barron's

- On holding through volatility: Capturing the asymmetrical returns of growth stocks requires holding the winners through thick and thin, resisting the urge to sell during temporary downturns. — Source: The Money Masters

- On rejecting groupthink: Discipline means relying on primary research rather than the prevailing sentiment of Wall Street prognosticators. — Source: T. Rowe Price: The Man, The Company, and The Investment Philosophy

- On avoiding the herd: Price's entire firm was built on doing independent primary research rather than consuming Wall Street research reports. — Source: T. Rowe Price Associates History

- On structural advantages: Long-term investing naturally reduces the drag of taxes and trading costs, providing a structural advantage over frequent trading. — Source: The Money Masters

Part 8: Ethics, Fees, and Client Alignment

- On the primary directive: "If you treat the customer right, he will reward you in the long term." — Source: T. Rowe Price: The Man, The Company, and The Investment Philosophy

- On aligned incentives: Price popularized the fee-based model over commissions because he believed a firm should only make more money if the client's portfolio actually grows. — Source: T. Rowe Price Associates History

- On mutual success: His fee structure was designed around a simple premise: "When our clients succeed, the firm succeeds." — Source: T. Rowe Price Associates History

- On the danger of commissions: Price left his early brokerage job because he found that transaction-based commissions incentivized churning accounts rather than sound, long-term investing. — Source: T. Rowe Price: The Man, The Company, and The Investment Philosophy

- On the no-load revolution: By removing heavy front-end sales loads, Price allowed clients to keep more of their initial capital working in the market. — Source: T. Rowe Price Associates History

- On transparency: He viewed the investment business as a profession of trust, requiring straightforward pricing and open communication with clients. — Source: T. Rowe Price: The Man, The Company, and The Investment Philosophy

- On reputational capital: Price recognized that an investment firm's goodwill and reputation for integrity was its most valuable—and most fragile—asset. — Source: T. Rowe Price: The Man, The Company, and The Investment Philosophy

- On protecting the client: "The only protection [for the client] was to select stocks whose earnings were growing faster than the overall economy." — Source: The Money Masters

- On legacy: Price built his firm as a fiduciary gold standard, prioritizing deep research and client defense above rapid asset gathering. — Source: T. Rowe Price: The Man, The Company, and The Investment Philosophy