Lessons from Todd Combs

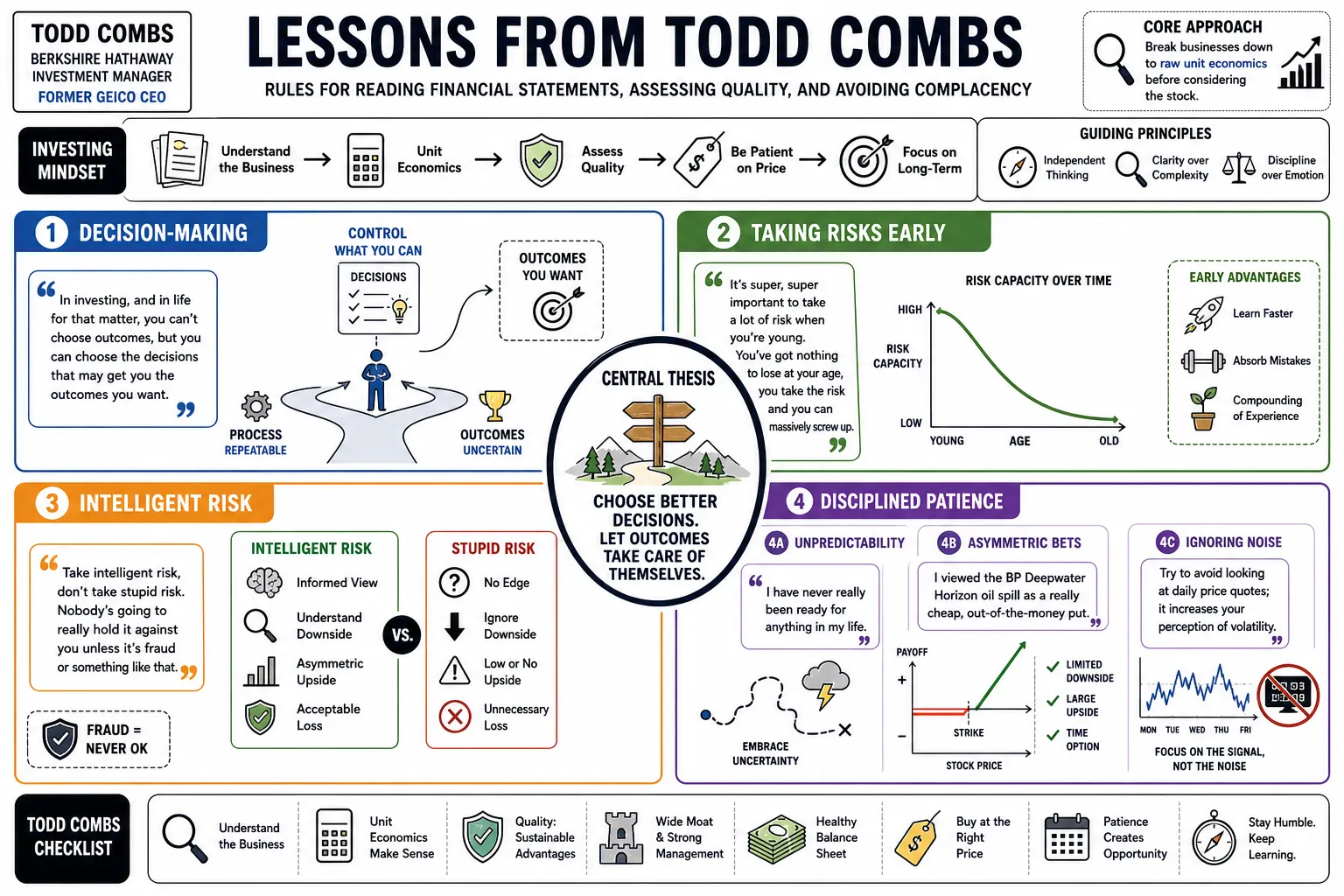

Berkshire Hathaway investment manager and former GEICO CEO Todd Combs analyzes businesses by breaking them down to their raw unit economics before considering the stock. This collection outlines his rules for reading financial statements, assessing a company's quality, and avoiding complacency.

Part 1: Risk & Decision Making

- On Decision-Making: "In investing, and in life for that matter, you can't choose outcomes, but you can choose the decisions that may get you the outcomes you want." — Source: [The Rational Walk]

- On Taking Risks Early: "It's super, super important to take a lot of risk when you're young. You've got nothing to lose at your age, you take the risk and you can massively screw up." — Source: [Business Insider]

- On Intelligent Risk: "Take intelligent risk, don't take stupid risk. Nobody's going to really hold it against you unless it's fraud or something like that." — Source: [Business Insider]

- On Unpredictability: "I have never really been ready for anything in my life." — Source: [Colossus]

- On Asymmetric Bets: "I viewed the BP Deepwater Horizon oil spill as a really cheap, out-of-the-money put." — Source: [Kingswell]

- On Ignoring Noise: "Try to avoid looking at daily price quotes; it increases your perception of volatility and makes for a more stressful, less rational experience." — Source: [The Rational Walk]

- On Taking the Initiative: "If you want to meet someone, figure out how to be helpful to them first and cold call them." — Source: [I Am Home Podcast]

- On The Multiplier Effect: "If any single factor in a business—quality, management, or price—is zero, the entire investment lacks merit." — Source: [Sahm Capital]

- On Emotional Control: "You need the temperament to grab ideas and do sensible things when you find them." — Source: [Kingswell]

- On Patience: "Most people fail to act on the right information even when they encounter it because they lack the temperament to wait out the cycle." — Source: [Kingswell]

Part 2: Business Analysis & The Research Sequence

- On Jigsaw Puzzles: "What do you do with a jigsaw puzzle? You dump out all the pieces and you start with the edges and the corners. You don't start in the middle and build your way out." — Source: [Business Insider]

- On Financial Statements: "Always focus on the cash flow statement first, then the balance sheet, and finally the income statement." — Source: [Sahm Capital]

- On the Income Statement: "The income statement is the most easily manipulated document in financial reporting." — Source: [Sahm Capital]

- On Retained Earnings: "You need to look at ten years of data to truly understand the relationship between retained earnings, debt, and growth." — Source: [Sahm Capital]

- On Short Selling: "Have a short seller's eye; be skeptical and willing to rip a company down to its studs to truly understand its operations." — Source: [Business Insider]

- On Spreadsheets: "A spreadsheet is not business reality. It is a representation that can often mislead." — Source: [The Rational Walk]

- On the Five-Year Test: "Ask yourself what level of confidence you have in predicting a company’s performance five years into the future." — Source: [Daniel Scrivner]

- On Progress: "Very few S&P 500 companies actually become 'better' businesses over a five-year period." — Source: [Value Research Online]

- On Reassembling the Pieces: "Once you tear a business down to its studs, see if you can put it back together and still like what you see." — Source: [Columbia Business School]

- On Assessing Moats: "We frequently, often daily, analyze whether the competitive moat of our businesses is widening or narrowing." — Source: [Daniel Scrivner]

Part 3: Quality & The Multiplicative Formula

- On Evaluating Investments: "I use a multiplicative formula: Quality Companies times Excellent Management times Reasonable Prices." — Source: [Sahm Capital]

- On Great Businesses: "Find one or two great businesses rather than over-diversifying your portfolio." — Source: [Worldly Partners]

- On What Makes a Good Business: "A good business is defined by the longevity of the company and the unquestionable quality of its financial statements." — Source: [The Motley Fool]

- On Price vs. Value: "I prefer to look at investments without knowing the price initially to avoid bias." — Source: [Masters Invest]

- On Management Quality: "Excellent management is a multiplier, but it cannot save a fundamentally flawed business model." — Source: [Sahm Capital]

- On the Quality Multiplier: "These evaluation factors are not additive; they multiply, meaning a zero anywhere ruins the whole equation." — Source: [Sahm Capital]

- On Apple: "When we evaluated Apple in 2016, we asked questions focused heavily on customer retention and the ecosystem's stickiness." — Source: [Value Research Online]

- On Avoiding Craziness: "Avoid seductive craziness in the market; stick to what is simple and understandable." — Source: [Benzinga]

- On True Value: "True value isn't found in what a company is doing today, but in what its moat will protect tomorrow." — Source: [Kingswell]

- On Moat Trajectory: "It doesn't matter how wide the moat is if the trajectory is negative." — Source: [Daniel Scrivner]

Part 4: Life & Complacency

- On Complacency: "People usually rise to their level of complacency." — Source: [Business Insider]

- On Limiting Factors: "If your dream is to make it to manager and you're perfectly fine there, that's pretty much where you're going to stop. People create their own limiting factors." — Source: [Business Insider]

- On Reading: "Reading 500 pages a week, not a day, is a more realistic and attainable benchmark for serious study." — Source: [The Rational Walk]

- On the Compounding of Knowledge: "Knowledge compounds like interest; the more you read, the more connections you make." — Source: [Farnam Street]

- On Reading Material: "My reading material is a complete hodgepodge, but it heavily indexes toward SEC filings." — Source: [The Rational Walk]

- On Doing the Work: "Reading alone is insufficient if you do not have the drive to execute on the ideas you find." — Source: [The Rational Walk]

- On Continuous Learning: "You must approach learning as a lifelong task; you are never truly done figuring out how the world works." — Source: [I Am Home Podcast]

- On Curiosity: "Curiosity is the engine that drives any successful investor to look where others are not looking." — Source: [Colossus]

- On Intellectual Humility: "You have to know what you do not know, and be perfectly fine leaving those puzzles unsolved." — Source: [Kingswell]

Part 5: Leadership & Management

- On Corporate Turnarounds: "A turnaround requires addressing the hard, unit-level economics before worrying about the macro picture." — Source: [Morningstar]

- On Remorseless Rationality: "To lead effectively, you must operate with remorseless rationality, especially when the decisions are unpopular." — Source: [Frederik's Journals]

- On Efficiency: "Reshaping a long-held gem often requires major repolishing and a ruthless focus on modernization." — Source: [The Motley Fool]

- On Employee Focus: "A company's culture must eventually align with its financial reality, even if that alignment is painful in the short term." — Source: [Business Insider]

- On Decentralization: "Trusting your deputies and avoiding the urge to constantly quiz them is the hallmark of a great decentralized structure." — Source: [Steady Compounding]

- On Operational Rigor: "You have to understand a business at the granular level before you can manage it at the executive level." — Source: [The Rational Walk]

- On Leading Through Crisis: "During a crisis, swift action to adjust pricing and give back to customers builds long-term trust." — Source: [The Motley Fool]

- On Truth in Leadership: "As a leader, your primary job is to seek the truth, no matter how ugly it might look on a spreadsheet." — Source: [Columbia Business School]

- On the Importance of the Edge: "Good leadership is about defining the edges of the puzzle clearly for your team." — Source: [Colossus]

Part 6: Learning from Munger & Buffett

- On Charlie Munger: "Charlie made it look so easy that it was almost as if he was born with the understanding of these concepts at birth." — Source: [Kingswell]

- On Behavioral Economics: "Reread 'Thinking, Fast and Slow' annually to keep your behavioral biases in check." — Source: [Kingswell]

- On Munger's Attention Span: "Munger possessed a long attention span that allowed him to wait out almost any market cycle." — Source: [Frederik's Journals]

- On the Power of the Cold Call: "Munger taught me that if you have something intelligent to say, reaching out directly is rarely a mistake." — Source: [Business Insider]

- On Integrity: "Buffett and Munger proved that being a model of integrity is actually a competitive advantage in finance." — Source: [Business Insider]

- On Autonomy: "Warren never asks me what I'm buying or selling; the trust is absolute once you are inside the tent." — Source: [Steady Compounding]

- On Simplicity: "The most profound lesson from Omaha is that investing is inherently simple, though it is never easy." — Source: [The Rational Walk]

- On Rationality: "Rationality is not something you turn on and off; it is a lens through which you must view every aspect of life." — Source: [Columbia Business School]

- On Long-Term Thinking: "Thinking in decades rather than quarters is the only way to avoid the seductive craziness of Wall Street." — Source: [Worldly Partners]

Part 7: Unit Economics & Details

- On the Granular Level: "You must understand performance at the unit level—a single store, a single subscriber, or a single policy." — Source: [The Rational Walk]

- On Consolidated Statements: "Consolidated financial statements often hide the true operational reality of a business." — Source: [Sahm Capital]

- On Insurance: "In insurance, understanding the cost of a single claim and the pricing of a single policy is the entire ballgame." — Source: [The Motley Fool]

- On the Real Business: "If you cannot explain the economics of one transaction, you cannot explain the business." — Source: [Kingswell]

- On Margins: "Top-line growth is a vanity metric if the unit-level margins are deteriorating." — Source: [Daniel Scrivner]

- On Scale: "Scaling a bad unit economic model just means you lose money faster." — Source: [Columbia Business School]

- On Consumer Behavior: "Look at the unit economics to tell you what the consumer actually values, not what the management team says they value." — Source: [The Rational Walk]

- On Capital Allocation: "Capital should only be allocated to units that have proven their economic viability in the real world." — Source: [Colossus]

- On the Retail Model: "In retail, you live and die by the four walls of a single store; if that doesn't work, nothing else matters." — Source: [I Am Home Podcast]

Part 8: Philosophy of Learning

- On the Liberal Arts: "Investing is the last liberal art; it requires you to synthesize information from wildly disparate fields." — Source: [Colossus]

- On Synthesizing Information: "The goal of reading isn't to memorize facts, but to build a framework where new facts can logically reside." — Source: [Farnam Street]

- On Changing Your Mind: "You must have the flexibility to destroy your best-loved ideas when the facts change." — Source: [Kingswell]

- On Information Flow: "Control your information flow carefully; a diet of junk information will yield junk decisions." — Source: [The Rational Walk]

- On the Value of History: "Studying the history of business failures is far more instructive than studying the successes." — Source: [Worldly Partners]

- On the Edges of Knowledge: "Knowing exactly where your edge ends is more important than how far it extends." — Source: [Columbia Business School]

- On the Jigsaw Metaphor: "Every new book you read is another piece of the jigsaw puzzle; eventually, the picture reveals itself." — Source: [Business Insider]

- On Asking Questions: "The quality of your investment decisions is directly correlated to the quality of the questions you ask the data." — Source: [Daniel Scrivner]

- On the Ultimate Goal: "The ultimate goal is not to be right on every stock, but to have a process that guarantees you won't be ruinously wrong." — Source: [I Am Home Podcast]