Lessons from Alex Rampell

Alex Rampell is a General Partner at Andreessen Horowitz who previously founded TrialPay and Affirm. He is known for mapping how traditional financial services are absorbed into technology products, and for articulating why startups must find distribution before incumbents replicate their ideas. This collection organizes his observations on banking moats, lending math, and why the next era of software companies will sell automated labor rather than software seats.

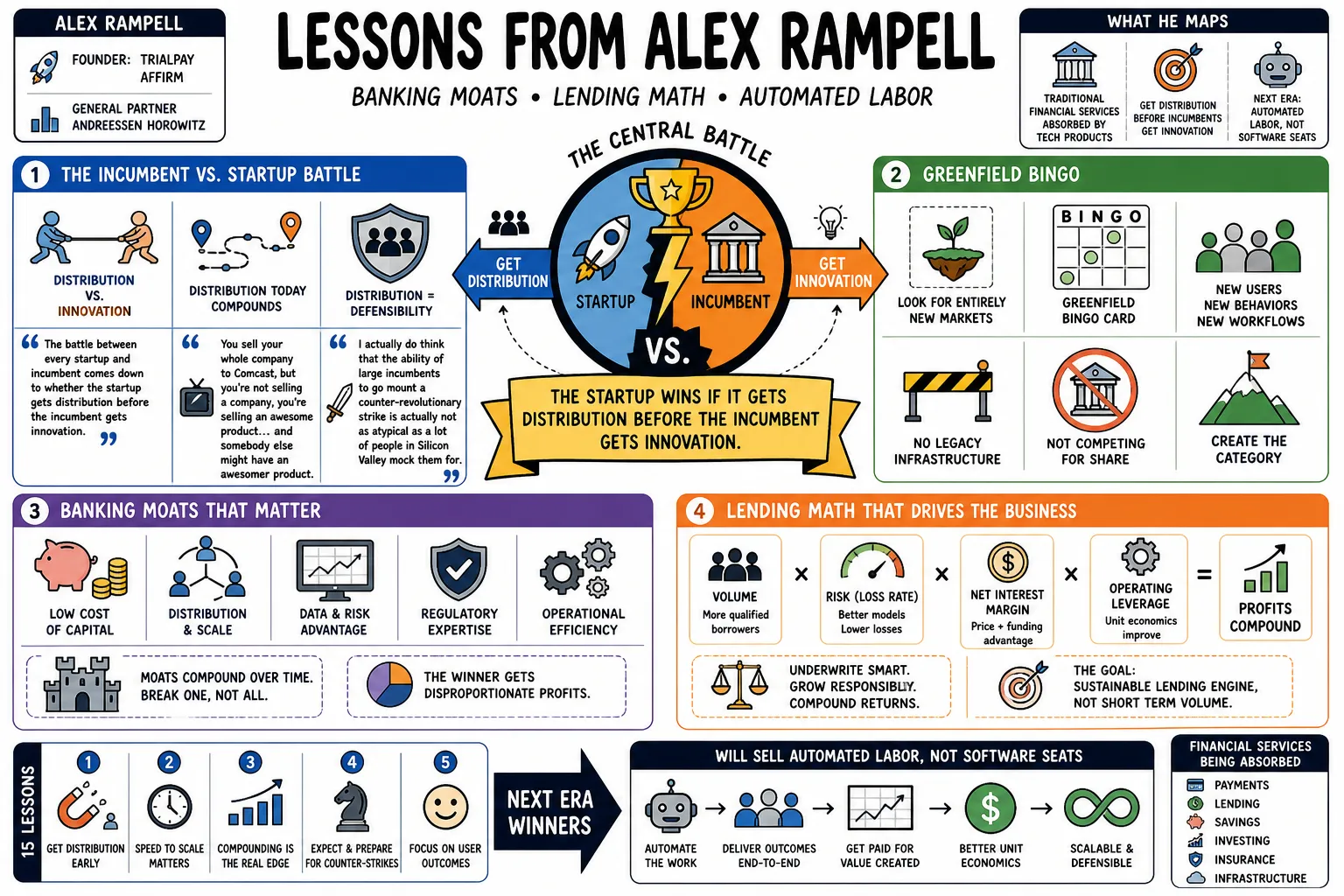

Part 1: The Incumbent vs. Startup Battle

- On the central battle: "The battle between every startup and incumbent comes down to whether the startup gets distribution before the incumbent gets innovation." — Source: [a16z]

- On the TiVo problem: "You sell your whole company to Comcast, but you're not selling a company, you're selling an awesome product... and somebody else might have an awesomer product." — Source: [Alex Rampell]

- On counter-revolutionary strikes: "I actually do think that the ability of large incumbents to go mount a counter-revolutionary strike is actually not as atypical as a lot of people in Silicon Valley mock them for." — Source: [Deciphr.ai]

- On Greenfield Bingo: Startups should look for entirely new markets created by technological shifts rather than playing a disruptive game of catch-up against massive organizations. — Source: [20VC]

- On the death of the middle: In venture capital and business broadly, you must either be a massive generalist with huge resources or a deep niche specialist; mid-sized generalists are being squeezed out. — Source: [20VC]

- On Operation Chokepoint 3.0: Private banks are engaging in Chokepoint 3.0 by charging extremely high fees to fintech apps for API access to basic customer routing data to block competition. — Source: [a16z]

- On banking moats: If a traditional bank charges a consumer $10 to move $100 into a crypto account, it essentially kills consumer choice through manufactured transaction friction. — Source: [Bitcoin.com]

- On protecting incumbents: The biggest obstacle to defeating a financial incumbent usually isn't technology; it's the entrenched bank's massively lower cost of capital. — Source: [a16z Podcast: Fintech for Startups and Incumbents]

- On infrastructure debt: Financial institutions are sitting on decades of infrastructure debt, which makes layering artificial intelligence on top of their core systems a dead end. — Source: [Pulse 2.0]

- On tech buzzwords: "A lot of people that say, 'I want a blockchain,' are the same people that a few years ago were saying, 'We want big data,' which in a couple of years will be saying, 'Oh, AI is very important to us.'" — Source: [Deciphr.ai]

Part 2: Systems of Record & The "Hostage" Dynamic

- On customer retention: "The best companies often have hostages, not customers — and they will maintain pricing irrespective of AI usage." — Source: [Alex Rampell]

- On positive selection: The ultimate framework for investing is finding a company that acts as an operating system or system of record that the business absolutely cannot live without. — Source: [Colossus]

- On atomic units: A system of record is the software that keeps track of the atomic units of a business, like Salesforce for opportunities or Workday for human resources. — Source: [a16z]

- On switching costs: Because systems of record sit at the center of a business's operational universe, the risk of switching is so high that businesses will keep paying for a mediocre incumbent. — Source: [Alex Rampell]

- On the presentation layer: The company controlling the interface the customer actually sees holds the most power, threatening to commoditize any middleware layer below it. — Source: [Colossus]

- On digital filing cabinets: For the last two decades, the SaaS playbook was building a digital filing cabinet for data previously kept on paper, and charging a monthly fee per seat. — Source: [AI Launchpad]

- On pricing power: When you move from being a digital filing cabinet to an active system of action, you shift from seat-based pricing to outcome-based pricing. — Source: [AI Launchpad]

- On holding maturity: "If you are, say, an unprofitable startup investing your cash, do not invest in long-maturity products — it doesn't matter how safe they are." — Source: [Alex Rampell]

- On horizontal systems: When horizontal giants try to serve every industry moderately well, they leave massive vulnerabilities for specialized, vertical operating systems to exploit. — Source: [a16z]

- On infrastructure as a moat: Companies like Stripe or AWS become so deeply embedded in other businesses that they act as the permanent plumbing of the internet. — Source: [Colossus]

Part 3: Fintech Fundamentals & The Math of Lending

- On first principles of lending: "If you ask me to loan you $100, and I think there's a 50% chance you don't pay me back, I should only make the loan if I get $200 back. Otherwise, I shouldn't make the loan!" — Source: [Alex Rampell]

- On restricting credit: If policymakers want to outlaw mathematically necessary high APRs for risky borrowers, they must accept that they are choosing to restrict access to credit entirely. — Source: [Alex Rampell]

- On adverse selection in speed: "If a company says, 'We'll underwrite you on the spot in one minute, no blood test,' that's going to be adverse selection. That's like, 'Ooh, I think I'm gonna die soon... I'm going to that company.'" — Source: [Reddit]

- On the game theory of insurance: Insurance product design is ultimately a game-theoretic struggle against adverse selection between the insurer and the insured. — Source: [Zac Townsend]

- On cross-collateralization: The future of banking lies in underwriting the whole customer and utilizing cross-collateralization among various financial products to lower risk and price. — Source: [Medium]

- On the cost to serve: A major bank might turn down a $400 loan not because the borrower is too risky, but simply because the operational cost to originate it makes it unprofitable. — Source: [a16z Podcast: Fintech for Startups and Incumbents]

- On embedded lending: By embedding a lending product directly into a software system like Square, the provider gets captive rights to that merchant base for cash advances based on perfect transaction data. — Source: [a16z Podcast: Fintech for Startups and Incumbents]

- On the evolution of the term: "In twenty years you would think about it as your bank, your insurance, your retirement account, you wouldn't necessarily think of it as your FinTech company." — Source: [The Waiter's Pad]

- On banking and trust: "Banking isn't about money. Banking is about trust." Technology can move money instantly, but building branch-level consumer trust is the hardest hurdle for a startup. — Source: [The Waiter's Pad]

Part 4: O2O Commerce & Real Estate (Friction Removal)

- On defining O2O: "The key to O2O is that it finds consumers online and brings them into real-world stores. It is a combination of payment model and foot traffic generator." — Source: [BSU]

- On Service as a SKU: The ultimate O2O opportunity is tacking barcodes onto un-warehousable physical services by standardizing them into a unit that can be sold like a product. — Source: [BSU]

- On measuring intent: O2O is inherently measurable because the payment or reservation begins online before the physical interaction occurs. — Source: [BSU]

- On the ketchup and fries strategy: "The best place to sell ketchup is when somebody's buying fries... selling to somebody at the point of another transaction where the intent is almost self-evident." — Source: [Alex Rampell]

- On real estate friction: Buying a home is the pinnacle of the American dream, yet it is a painful, convoluted process full of brokers, banks, notaries, and title insurers. — Source: [Dokumen]

- On agent economics: "Real estate is a weird business. There are two million real estate agents... The median number of homes sold is two, the modal number of homes sold is zero." — Source: [Dokumen]

- On the 6 percent fee: The fixed real estate agent commission is a massive $90 billion market friction that is structurally fragile and heavily exposed to software intervention. — Source: [a16z]

- On institutional counterparties: "In the future, you will buy your house from, or sell your house to, a company" instead of engaging in an inefficient peer-to-peer transaction. — Source: [WikiCasa]

- On data vs human agents: Humans can look at comps, but they lack a data science team to algorithmically determine the exact best month to list a property; computers do this fundamentally better. — Source: [Dokumen]

Part 5: Vertical Software & "Drinking the Milkshake"

- On the Daniel Plainview strategy: "Like Daniel Plainview’s oil strategy, vertical software companies looking to disrupt established players must strategically position themselves to extract value." — Source: [a16z]

- On drinking the milkshake: By acting as the primary workflow tool for an industry, vertical startups capture offline data and effectively drain the value from legacy horizontal platforms. — Source: [a16z]

- On software as a wedge: "The second wave, cloud + fintech, increased revenue by enabling VSaaS companies to embed financial services... Software is the wedge, but the business model is often fintech." — Source: [Milled]

- On going boring: The best answer is often to go boring; merchants didn't want flashy products, they wanted cheap, commoditized core payment processing that just worked. — Source: [Alex Rampell]

- On embedded finance: Every company that has a high-frequency relationship with a customer will inevitably become a fintech company by offering native financial services. — Source: [Alex Rampell]

- On full-stack evolution: For a technology company to truly disrupt a physical category like restaurants, it must move past being a search portal to becoming a full-stack participant in the transaction. — Source: [WikiCasa]

- On overestimating data moats: "In my experience... people overestimate the value of data from the perspective of building a competitive advantage or moat." — Source: [Square Peg]

- On LLM parity: If your proprietary data closely resembles the base data a language model was trained on, it won't yield a performance increase large enough to fend off competitors. — Source: [Square Peg]

- On vertical operating systems: A vertical OS bundles multiple discrete systems of record into one unified platform tailored specifically to one industry, massively increasing its defensibility. — Source: [a16z]

Part 6: Visa, Protocols, and Networks

- On protocol vs legal design: "A well-thought-through protocol is more valuable and protective than lawyers, contracts, and even governments — it will survive all of them." — Source: [Alex Rampell]

- On decentralized preservation: Decentralized networks preserve true independence by ensuring value accrues to the network participants rather than a central toll-taker. — Source: [Alex Rampell]

- On Visa's origin: Visa is the original protocol business—a communication standard that allowed essentially all banks in the world to seamlessly authorize and clear transactions. — Source: [Scribd]

- On the protocol effect: "Once you build a standard way for lots of companies to communicate information with one another, a protocol, it's incredibly hard to change or disrupt." — Source: [Scribd]

- On the tragedy of centralization: Because the Visa protocol was eventually enshrined in a for-profit entity, the central actor now holds more value than the network participants who created it. — Source: [Alex Rampell]

- On alternative payment networks: Buy Now, Pay Later is not just a loan, but a new protocol that aligns merchant and consumer incentives while entirely bypassing traditional credit card rails. — Source: [Colossus]

- On the data network effect: A true data network effect occurs only when adding a new user mathematically improves the experience for all other users, rather than simply creating a larger static database. — Source: [20VC]

- On blockchain utility: The test for whether a blockchain application is valid is determining if the specific utility is fundamentally optimized by a decentralized database rather than a centralized one. — Source: [20VC]

- On the private blockchain paradox: "Despite a lot of 'private blockchain' nonsense out there, this is a great example of how Visa could have or should have been constructed... to ensure perpetual independence." — Source: [Alex Rampell]

Part 7: Founder Psychology & The Materialization Framework

- On the Trifecta of Materialization: "You want to invest in people that can materialize labor, capital, and customers." — Source: [Wave]

- On materializing labor: The first test of an entrepreneur is whether they can convince highly competent people to leave secure, high-paying jobs to work on a risky idea. — Source: [Wave]

- On materializing capital: A founder must be able to craft a compelling narrative that convinces investors to provide the fuel to build the business. — Source: [Wave]

- On materializing customers: The final pillar is the sheer agency required to convince people to buy or adopt a product that barely exists yet. — Source: [Wave]

- On the Count of Monte Cristo: Rampell looks for founders with a mentality matching the Count of Monte Cristo—a deep, obsessive desire for revenge or redemption against past slights. — Source: [Wave]

- On the strongest motivator: "The most powerful motivator I have ever seen is not money, it's revenge." — Source: [a16z Podcast: Fintech for Startups and Incumbents]

- On conviction vs consensus: "Conviction beats consensus." The best startup investments are usually ideas that most people reject but one passionate person holds with absolute certainty. — Source: [Wave]

- On founder agency: The best founders possess an extreme level of agency; they don't wait for permission or perfect conditions, they simply will their companies into existence. — Source: [Podwise]

- On historical study: The greatest operators have deeply studied the history of their category to understand why previous attempts succeeded or failed. — Source: [Podwise]

Part 8: AI as Labor & The Future of Software

- On the new TAM: "The software itself can actually do the work. Therefore the market opportunity for software today is no longer just IT spend; it's largely labor." — Source: [a16z]

- On software as labor: "Software becomes labor. It’s the new E=MC². Capital buys coffee, engineers, and GPUs. Out comes code that takes the role of labor." — Source: [Milled]

- On eroding bank moats: Generative AI will erode the friction that allows big banks to pay low interest on deposits, as AI agents will automatically shop and move money for consumers. — Source: [Alex Rampell]

- On the SKU-ification of Labor: Tasks that once required hiring an employee are shifting to buying a discrete AI service via credit card, massively expanding digital payment volumes. — Source: [Alex Rampell]

- On moving from record to action: Software is evolving from a passive system of record that stores data for a human, into a system of action that performs the task autonomously. — Source: [AI Launchpad]

- On the 13 trillion prize: The global software market is worth roughly $300 billion, but the global labor market is $13 trillion; AI allows software to capture the latter. — Source: [AI Launchpad]

- On the speed of AI development: Because AI has compressed software build times from years down to weeks, the application layer is hyper-competitive, making distribution moats more vital than ever. — Source: [Podwise]

- On new credit underwriting: Incorporating machine learning and cash-flow data has finally enabled credit models to expand access to populations with thin or non-existent credit files. — Source: [FinRegLab]

- On errors of omission: "Errors of omission are much bigger than errors of commission." Missing a generational technology platform is far worse than losing money on a failed bet. — Source: [Frankfurt School]

- On market inflection points: "The key thing is finding the inflection point where there still is interest, where there's some notion of pull from the consumer, but it's no longer so crowded that it's effectively overfished." — Source: [a16z]