Lessons from Jay Hoag

As the founding general partner of Technology Crossover Ventures and chairman of Netflix, Jay Hoag built a career backing tech companies from their private stages straight into the public markets. This profile covers his methods for holding through volatility, assessing founders, and ignoring market hype.

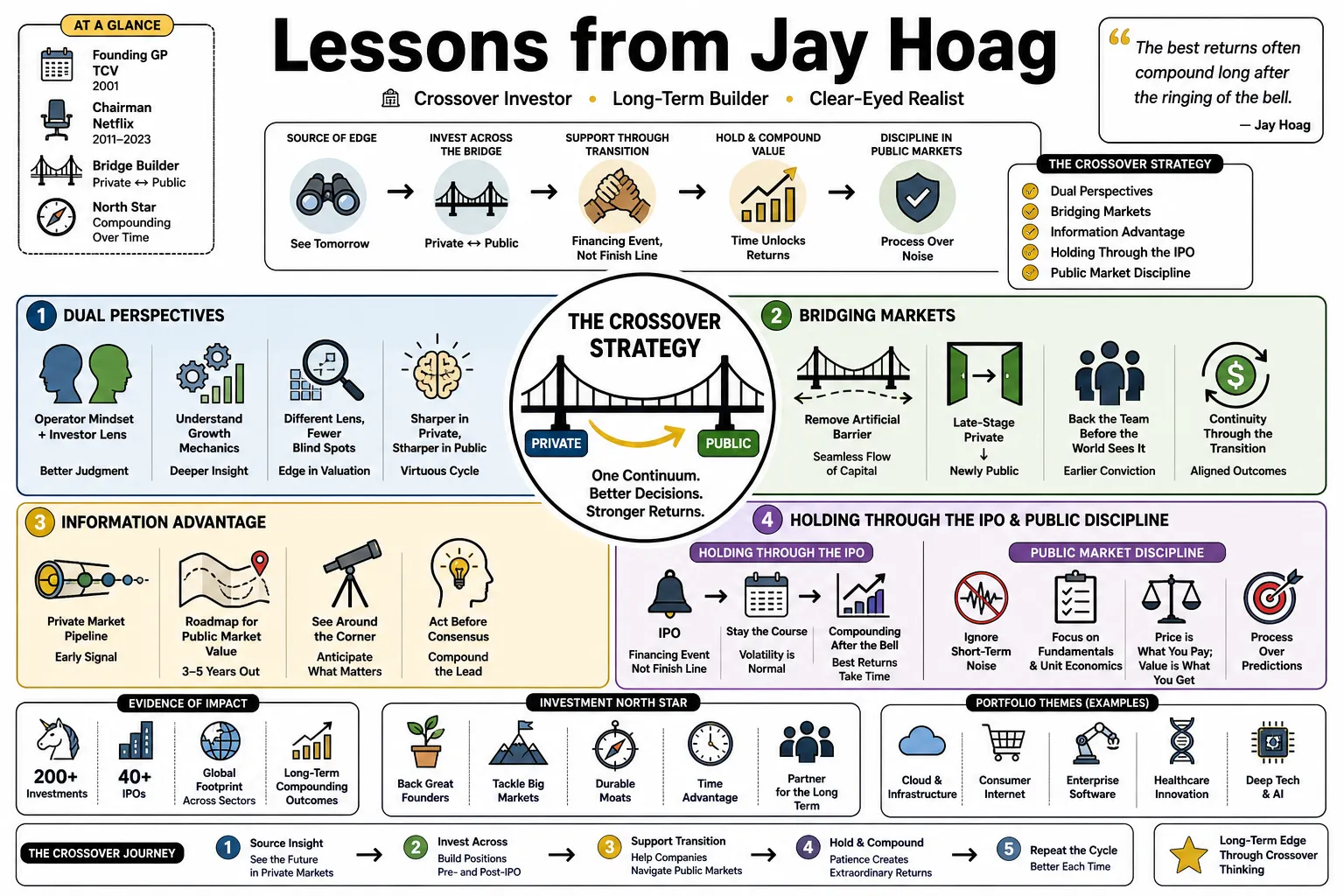

Part 1: The Crossover Strategy

- On Dual Perspectives: "Operating as a private investor intrinsically makes you a sharper public market investor, as you understand the foundational mechanics of growth." — Source: Invest Like the Best

- On Bridging Markets: "The original thesis of TCV was to remove the artificial barrier between late-stage private companies and newly public ones, allowing capital to flow seamlessly across the transition." — Source: Acquired Podcast

- On Information Advantage: "Seeing the private market pipeline gives you a roadmap for what public markets will value three to five years down the line." — Source: TCV Website

- On Holding Through the IPO: "Going public is merely a financing event, not a finish line; the best returns often compound long after the ringing of the bell." — Source: Invest Like the Best

- On Public Market Discipline: Hoag treats public-market pressure as useful when it forces companies to focus on funding, product value, customer delight, and the durability of the business rather than on short-term headlines. — Reference: Acquired interview with Jay Hoag

- On Flexibility: "A crossover fund isn't forced to exit a winner simply because their equity structure changes from private to public." — Source: Acquired Podcast

- On Synergistic Insights: "You cannot accurately price a public tech company without deeply understanding the private startups aiming to disrupt it." — Source: Invest Like the Best

- On Capital Structure: "By being agnostic to whether a company is public or private, you focus purely on the durability of the business model rather than the mechanics of the trade." — Source: TCV Website

- On The 1995 Thesis: "When we started in 1995, the idea that one firm could hold a company from its Series C through its tenth year as a public entity was unorthodox; now it is a recognized advantage." — Source: Acquired Podcast

Part 2: Contrarian Investing (Avoiding the Herd)

- On Momentum Investing: "Money sort of chases momentum or follows perceived momentum. At the risk of insult, possibly like 7-year-olds playing soccer, the ball goes over there, everybody goes over there." — Source: Business Insider

- On AI Hype: "The rush into every AI derivative without examining the underlying unit economics is a classic example of herd mentality blinding basic diligence." — Source: Invest Like the Best

- On Being Misunderstood: Hoag says investors buying under severe public pressure must be willing to look wrong for a while, but only when conviction is grounded in the team, product, customer delight, moats, and execution. — Reference: Acquired interview with Jay Hoag

- On Out-of-Favor Sectors: "Often the best entry points are found in consumer internet businesses when the broader venture community has pivoted entirely to enterprise software." — Source: Invest Like the Best

- On the Dot-Com Bubble: "Looking back, I think everybody throughout the system, ourselves included, made mistakes by temporarily ignoring fundamental business physics." — Source: PBS FRONTLINE

- On Recognizing Danger: "When you see investors backing companies wildly outside of their core expertise, everyone should step back and say, run for the hills, these are danger signs." — Source: PBS FRONTLINE

- On Independent Conviction: "You cannot borrow someone else's conviction; if you only invest because a top-tier firm is leading the round, you will panic when they panic." — Source: Acquired Podcast

- On Price Discipline: "The hardest discipline in a bull market is walking away from a great company simply because the valuation requires a suspension of disbelief." — Source: TCV Website

- On Patience: Hoag frames contrarian investing as the discipline to reassess a company dispassionately during market dislocations instead of letting temporary headlines replace the underlying business analysis. — Reference: Acquired interview with Jay Hoag

- On Ostracization: "Success in venture capital often requires the willingness to be temporarily ostracized by your peers for holding an unpopular thesis." — Source: Invest Like the Best

Part 3: Founders & Leadership

- On Crazy Founders: "The people who actually build enduring, category-defining companies usually have a vision that borders on the slightly crazy." — Source: Invest Like the Best

- On Founder Resilience: "Intelligence is common; the capacity to absorb massive, repeated psychological blows and keep operating is the rare trait we look for in CEOs." — Source: Acquired Podcast

- On Leadership Development: Hoag emphasizes that the CEO and team often determine whether TCV doubles down in stressed situations, because exceptional execution can separate companies with similar opportunities. — Reference: Acquired interview with Jay Hoag

- On Backing Teams: "We are fundamentally in the business of backing management teams for the long haul, knowing the product will inevitably change." — Source: TCV Website

- On Founder-Led Companies: "Founders possess a moral authority within their organizations that professional CEOs struggle to replicate, which is essential during severe pivots." — Source: Invest Like the Best

- On Evaluating Talent: "You want leaders who are exceptionally clear thinkers but also possess a quiet intensity that outlasts initial enthusiasm." — Source: Acquired Podcast

- On Honesty: Hoag advises leaders in pressured public companies to focus on the business, stay passionate about the roadmap, and keep delivering value to consumers rather than letting stock-price narratives dictate decisions. — Reference: Acquired interview with Jay Hoag

- On Evolving Roles: "A founder's job changes completely every time the company's headcount triples; those who cannot delegate will drown their own creation." — Source: TCV Website

- On Hiring: "A key metric of a leader is whether they are consistently able to recruit executives who are functionally better than they are." — Source: Invest Like the Best

Part 4: Long-Term Horizon (The Long Game)

- On Compounding: "The magic of technology investing is finding a compounding machine and leaving it alone, rather than trying to time the exit perfectly." — Source: Acquired Podcast

- On Board Tenure: "Staying on a board for over two decades isn't about maintaining control; it is about providing institutional memory as the company reinvents itself." — Source: Netflix Investor Relations

- On Time Arbitrage: "In a market hyper-focused on quarterly earnings, simply having a five-to-ten-year time horizon is a massive structural advantage." — Source: Invest Like the Best

- On Holding Winners: TCV's crossover model grew from the view that strong companies do not stop compounding when they go public, so investors should be able to remain long-term partners through the private-to-public transition. — Reference: TCV summary of Hoag on Acquired

- On IPOs as Milestones: "An initial public offering is a milestone of liquidity, not a capstone on growth. The work of building the business continues unabated." — Source: TCV Website

- On Patience Through Volatility: "If you truly believe in the unit economics and the management team, a fifty percent draw-down in the stock price is noise, not a signal to sell." — Source: Acquired Podcast

- On Sustained Growth: "We look for businesses that can maintain twenty-plus percent growth for a decade, which requires a constantly expanding total addressable market." — Source: Invest Like the Best

- On Enduring Value: "Fads generate rapid markups; enduring value is built slowly through superior customer retention and operational scaling." — Source: TCV Website

- On Relationship Building: Hoag's Netflix story shows the value of following exceptional entrepreneurs over many years, from Reed Hastings's earlier Pure Software experience through Netflix's later crises and reinventions. — Reference: Acquired interview with Jay Hoag

- On Long-Term Alignment: "When your fund structure allows you to hold public stock for years, your incentives perfectly align with the long-term vision of the founders." — Source: Acquired Podcast

Part 5: Rigorous Diligence & Valuation

- On Deep Diligence: "Diligence isn't about checking boxes; it is about uncovering the fundamental truth of how a company acquires and retains its customers." — Source: TCV Website

- On Unit Economics: "No amount of top-line hyper-growth can permanently obscure upside-down unit economics; the math eventually catches up." — Source: Invest Like the Best

- On Valuation Discipline: Hoag says difficult investments require repeatedly reassessing the CEO, team, product, customer delight, competitive moats, and execution rather than relying on market narratives alone. — Reference: Acquired interview with Jay Hoag

- On Customer Cohorts: "We spend an inordinate amount of time analyzing customer cohorts; if older cohorts aren't stabilizing and expanding, the growth is hollow." — Source: Acquired Podcast

- On Market Size: "It is much easier to model the current market than it is to accurately underwrite how a transformative product will expand that market." — Source: Invest Like the Best

- On Competitive Moats: "A true moat goes beyond a technological head start; it requires structural advantages in data, network effects, or scale that compound over time." — Source: TCV Website

- On Financial Physics: TCV describes Hoag's later Invest Like the Best conversation as a reflection on growth investing and the technology industry's evolution since TCV's founding, with attention to how strategy and timing can change. — Reference: TCV summary of Hoag on Invest Like the Best

- On Capital Efficiency: "We prefer companies that view capital as a tool for acceleration rather than a crutch for survival." — Source: Acquired Podcast

- On Signal vs. Noise: "Rigorous diligence is the mechanism by which you separate the actual signal of product-market fit from the noise of aggressive marketing spend." — Source: Invest Like the Best

Part 6: Navigating Cycles & Downturns

- On Market Cycles: "Every decade produces a new paradigm that investors claim repeals the laws of economics. They are always wrong." — Source: PBS FRONTLINE

- On Macro Downturns: "The truest test of a partnership is not how you celebrate the IPO, but how you support the founder when the macro environment collapses." — Source: Acquired Podcast

- On Staying the Course: "During severe volatility, the hardest and most important action is often doing absolutely nothing and trusting your initial underwriting." — Source: Invest Like the Best

- On Bear Markets: "Bear markets are where exceptional returns are seeded, as the lack of cheap capital starves irrational competitors and clears the field for category leaders." — Source: TCV Website

- On Panic: Hoag tells operators whose stocks are down sharply to avoid taking the market move personally, assume the business must still be well funded, and concentrate on the roadmap and consumer value. — Reference: Acquired interview with Jay Hoag

- On Rationalizing Cuts: "In a downturn, companies must ruthlessly prioritize. Survival requires cutting everything that doesn't directly serve the core customer." — Source: Acquired Podcast

- On Defensive Moats: "When the tide goes out, companies with high switching costs and mission-critical software are the ones left standing." — Source: Invest Like the Best

- On Opportunistic Capital: "Market dislocations provide the rare opportunity to acquire stakes in generational companies at prices that actually make mathematical sense." — Source: TCV Website

- On Navigating the Bubble: "The lesson of 2001 wasn't that the internet was a fad; it was that infrastructure takes time to catch up to ambition." — Source: PBS FRONTLINE

- On Resilience: Hoag points out that great technology companies often pass through moments of severe stress, from Netflix and Expedia to Airbnb, Zillow, and Facebook, and that survival through those periods can define the outcome. — Reference: Acquired interview with Jay Hoag

Part 7: Board Governance & Partnership

- On the Role of the Board: "A board's job is not to run the company. Its job is to hire the CEO, fire the CEO, and ask the difficult questions the executive team might be avoiding." — Source: Netflix Investor Relations

- On Behind-the-Scenes Support: "The best investors operate entirely behind the scenes; the spotlight belongs entirely to the founders and their operators." — Source: TCV Website

- On Challenging Founders: "You serve a founder best not by agreeing with them, but by respectfully stress-testing their assumptions in a private setting." — Source: Acquired Podcast

- On Board Transitions: "As a company moves from private to public, the board must evolve from a product-focused advisory group to one grounded in governance and audit rigor." — Source: Invest Like the Best

- On Institutional Memory: Netflix identifies Hoag as chairman and a director since 1999, which gives him unusually long board context across multiple company reinventions and market cycles. — Reference: Netflix investor-relations director profile

- On Navigating Crises: "In a crisis, a board must shift from oversight to active support, acting as a sounding board without micromanaging the operational response." — Source: TCV Website

- On Alignment of Interests: "The friction in most boardrooms stems from a misalignment of time horizons between the founders and short-term focused investors." — Source: Acquired Podcast

- On Trust: "If there is no baseline of absolute trust between the CEO and the lead independent director, the board architecture is functionally broken." — Source: Invest Like the Best

- On Managing Egos: Hoag's governance posture is less about public visibility than patient judgment: he describes TCV's role as long-term partnership through volatile public and private market conditions. — Reference: Acquired interview with Jay Hoag

Part 8: Market Opportunity & Category Definers

- On Category Creation: "The most lucrative investments aren't in companies taking market share in an existing category, but those actively defining a completely new one." — Source: Invest Like the Best

- On the Consumer Internet: "While others rush to SaaS, consumer internet remains compelling because the scale of global adoption allows for unprecedented winner-take-all dynamics." — Source: Acquired Podcast

- On Platform Shifts: "Generational companies are usually born at the exact intersection of a major platform shift and an unserved consumer need." — Source: TCV Website

- On TAM Expansion: Hoag describes Netflix's international opportunity as a case where investors could not simply extrapolate current data but could still reason from the product's broader consumer value proposition. — Reference: Acquired interview with Jay Hoag

- On Network Effects: "Once a business achieves structural network effects, the cost of customer acquisition plummets while the value to the user continuously rises." — Source: Invest Like the Best

- On Scaling Global: "To become a true category leader, a company must eventually prove its model can seamlessly cross geographic and cultural borders." — Source: TCV Website

- On Recognizing Patterns: "After looking at thousands of software companies, you develop a muscle memory for what an inevitable monopoly looks like in its early days." — Source: Acquired Podcast

- On Enduring Value: Hoag keeps returning to basic business quality: the team, product, customer delight, competitive moats, funding, and execution matter more than the market story around a company at any given moment. — Reference: Acquired interview with Jay Hoag

- On the Tech Ecosystem: "The technology sector isn't an isolated vertical anymore; it is the horizontal foundational layer that will eventually rewire every traditional industry on earth." — Source: Invest Like the Best