Lessons from Jeff Horing

Jeff Horing co-founded Insight Partners and grew it into a massive software investment firm by treating the industry as a predictable, math-driven business. He built his reputation on a systematic, high-volume approach to sourcing deals. This profile collects his practical frameworks for evaluating software economics, scaling startups, and navigating venture capital.

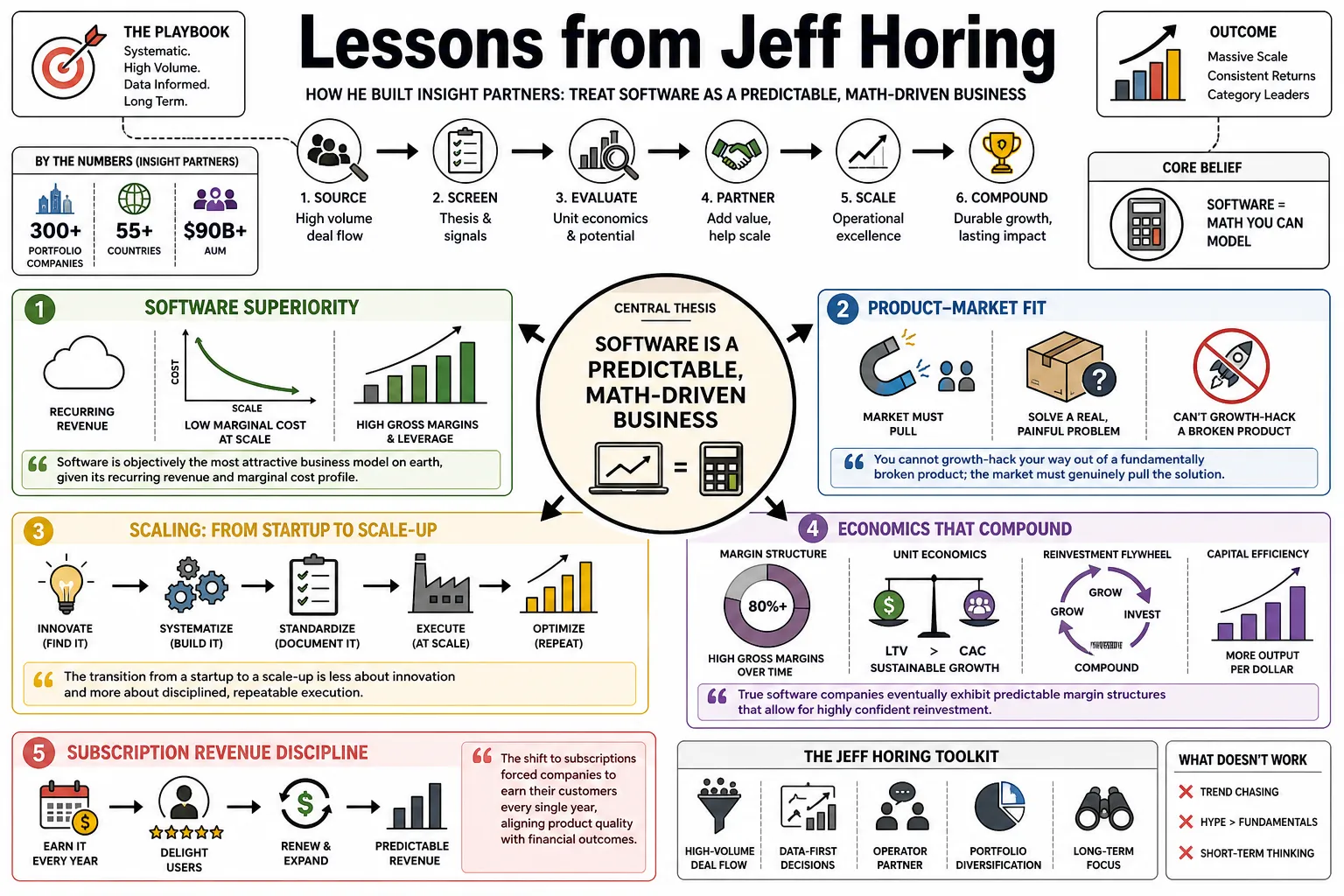

Part 1: The Software Business Model

- On Software Superiority: "Software is objectively the most attractive business model on earth, given its recurring revenue and marginal cost profile." — Source: [Insight Partners]

- On Product-Market Fit: "You cannot growth-hack your way out of a fundamentally broken product; the market must genuinely pull the solution from you." — Source: [Invest Like the Best]

- On Scaling: "The transition from a startup to a scale-up is less about innovation and more about disciplined, repeatable execution." — Source: [Startup for Startup]

- On Margin Structure: "True software companies eventually exhibit predictable margin structures that allow for highly confident reinvestment." — Source: [Insight Partners]

- On Subscription Revenue: "The shift to subscriptions forced companies to earn their customers every single year, aligning product quality with financial outcomes." — Source: [Invest Like the Best]

- On B2B Software: "Enterprise software is largely immune to the fleeting consumer trends that can wipe out other types of businesses overnight." — Source: [Insight Partners]

- On Defensibility: "A sticky software product integrated into a company's daily workflow becomes a nearly immovable asset." — Source: [Invest Like the Best]

- On Capital Efficiency: "The best software businesses require surprisingly little external capital once their fundamental economic engine is humming." — Source: [Startup for Startup]

- On APIs: "APIs have quickly become the fundamental building blocks of software used by developers in every industry, in every country across the globe." — Source: [YourStory]

- On Enduring Value: "We invest in software because the terminal value of a dominant platform is vastly underappreciated in early stages." — Source: [Insight Partners]

Part 2: The Sourcing Machine and Deal Flow

- On Systematic Outreach: "Our sourcing engine is built to eliminate serendipity; we want to map every relevant software company globally." — Source: [Invest Like the Best]

- On The Analyst Model: "Deploying a massive team of analysts to cold-call and research allows us to find companies years before they actively seek capital." — Source: [Invest Like the Best]

- On Pattern Recognition: "When you speak to thousands of founders a year, your pattern recognition for what constitutes a breakout success becomes institutionalized." — Source: [Invest Like the Best]

- On Early Contact: "The goal is to be the first institutional investor a founder thinks of when they finally decide they want to accelerate growth." — Source: [Insight Partners]

- On Volume: "Volume in sourcing isn't just about finding deals; it's about deeply understanding the baseline metrics of every sub-sector." — Source: [Invest Like the Best]

- On Deal Velocity: "A structured sourcing machine allows you to move with immense conviction when you finally find the right outlier." — Source: [Startup for Startup]

- On Bootstrapped Companies: "Some of the most capital-efficient, fundamentally sound businesses are the ones who ignored venture capital for the first five years." — Source: [Insight Partners]

- On Database Building: "Our internal database of software companies is perhaps our most valuable proprietary asset." — Source: [Invest Like the Best]

- On Consistency: "Deal flow cannot rely on the personal networks of a few partners; it must be an industrial, repeatable process." — Source: [Invest Like the Best]

Part 3: The One-Fund Strategy

- On Fund Structure: "Having a single fund prevents internal silos and ensures that the best opportunity gets funded, regardless of its stage." — Source: [Invest Like the Best]

- On Flexibility: "The market changes rapidly; a one-fund approach allows us to pivot from early-stage growth to late-stage buyouts without asking LPs for permission." — Source: [Insight Partners]

- On Alignment: "When everyone shares the same economics, you eliminate the politics of which partner’s specific fund is deploying capital." — Source: [Invest Like the Best]

- On Scale: "A massive, unified pool of capital allows us to support a founder from a Series A all the way through an IPO and beyond." — Source: [Startup for Startup]

- On Capital Allocation: "Capital should flow to the highest risk-adjusted return at any given moment, whether that’s a $10M check or a $500M check." — Source: [Invest Like the Best]

- On Contrarianism: "While others raised specialized funds for every niche, we found immense competitive advantage in doing the exact opposite." — Source: [Insight Partners]

- On Mega-Funds: "If I had $100 billion, that's what I would do because I think you could really differentiate yourself tremendously from the pack." — Source: [Invest Like the Best]

- On Market Cycles: "A unified fund structure is vastly more resilient during downturns because you aren't forced to deploy into a specific, overvalued stage." — Source: [Insight Partners]

- On Simplicity: "Complexity in fund structure usually serves the GP, not the LP or the founder. Keep the structure simple and focus on the investments." — Source: [Invest Like the Best]

Part 4: Operational Value-Add and Insight Onsite

- On Beyond Capital: "Money is a commodity; the true differentiator for a firm is the tactical, operational support you can inject into a portfolio company." — Source: [Insight Partners]

- On Scaling Sales: "Most founders are great at building product, but institutionalizing a go-to-market motion requires a completely different skill set." — Source: [Startup for Startup]

- On Insight Onsite: "We built an internal consulting firm of operators because founders need functional experts, not just board members." — Source: [Insight Partners]

- On Executive Hiring: "Helping a company transition from its founding team to seasoned executives is the highest-leverage activity an investor can perform." — Source: [Invest Like the Best]

- On Ego: "We don't have to be the loudest voice at the table ever. We want to be the most helpful voice at the table and we don't need credit for that help." — Source: [Invest Like the Best]

- On Pricing Strategy: "Optimizing pricing and packaging is often the fastest, least destructive way to immediately accelerate a software company's growth." — Source: [Insight Partners]

- On Playbooks: "There is no need to reinvent the wheel on SaaS metrics or compensation structures; we provide the playbooks so founders can focus on their unique product." — Source: [Startup for Startup]

- On M&A Support: "Programmatic M&A is a muscle most startups haven't developed; we step in to help them execute acquisitions effectively." — Source: [Insight Partners]

- On Operational Empathy: "Advice from a former operator who has actually built a sales comp plan is infinitely more valuable than theory from a finance professional." — Source: [Invest Like the Best]

Part 5: Metrics and College-Level Math

- On Gross Retention: "If a business's gross retention number is less than 90%, founders should seriously rethink their fundamental approach." — Source: [Calcalist]

- On Net vs. Gross Retention: "Net retention masks churn with upsells; gross retention is the raw, unvarnished truth about whether customers actually need your product." — Source: [Invest Like the Best]

- On College-Level Math: "Evaluating software economics shouldn't be based on gut feeling; it requires disciplined, college-level math to project unit economics at scale." — Source: [Invest Like the Best]

- On Predictability: "It was amazing what we continue to learn about metrics that really are the best predictors for future outcomes, which is really the dream." — Source: [Invest Like the Best]

- On Rule of 40: "The balance between growth rate and profit margin is the ultimate test of a software company's operational maturity." — Source: [Insight Partners]

- On Customer Acquisition Cost: "A low CAC is great, but a rapid CAC payback period is what actually dictates how fast you can safely burn capital." — Source: [Startup for Startup]

- On Churn: "High churn is a tax on growth. You are constantly filling a leaky bucket instead of building enterprise value." — Source: [Insight Partners]

- On Capital Efficiency Metrics: "We look deeply at how much ARR is generated per dollar of capital burned; it reveals the underlying physics of the business." — Source: [Invest Like the Best]

- On Financial Discipline: "Great software metrics don't happen by accident; they are the result of rigorous, uncompromising financial discipline across the organization." — Source: [Insight Partners]

- On Data Visibility: "A CEO who lacks immediate, granular visibility into their unit economics is driving blind in a fast-moving market." — Source: [Startup for Startup]

Part 6: Talent, Leadership, and Culture

- On Assessing Founders: "We look for a rare combination of intense drive, raw intellectual horsepower, and the humility to know what they don't know." — Source: [Startup for Startup]

- On Internal Training: "Initially we just threw people in the water to see how they swim, but scaling a firm requires institutionalized training programs." — Source: [Invest Like the Best]

- On Work Ethic: "There is no substitute for sheer diligence; the best investors and founders simply outwork their peers." — Source: [Insight Partners]

- On Judgment: "Analytical skills get you in the door, but the ability to exercise calm, decisive judgment under pressure is what makes a great partner." — Source: [Invest Like the Best]

- On Firm Culture: "A culture of high performance must be balanced with a culture of deep collaboration, or the organization will tear itself apart." — Source: [Insight Partners]

- On Hiring Mistakes: "Holding onto the wrong executive too long is the most common and damaging mistake we see fast-growing startups make." — Source: [Startup for Startup]

- On Board Dynamics: "A board's job is not to run the company, but to ensure the right CEO is in the seat and to challenge their assumptions rigorously." — Source: [Invest Like the Best]

- On Resilience: "The trajectory of a startup is never a straight line; the capacity to absorb massive shocks without losing focus is essential." — Source: [Insight Partners]

- On Intellectual Honesty: "You have to be willing to look at bad data and admit a thesis is broken, rather than twisting the math to fit your narrative." — Source: [Invest Like the Best]

Part 7: The Evolution of Venture and AI

- On AI as an Accelerator: "AI is fundamentally a TAM accelerator; it will vastly expand what software is capable of doing for legacy industries." — Source: [Invest Like the Best]

- On Blurring Lines: "The difference between software and service is going to look a lot more blurred as AI automates complex workflows." — Source: [Insight Partners]

- On Value Creation: "Buying cheap in technology, there's not a long list of really rich people who've done that. As compared to the people who've just bought the Dream." — Source: [Invest Like the Best]

- On Market Maturation: "The software industry is transitioning from its hyper-growth adolescence into a mature, deeply institutionalized asset class." — Source: [Insight Partners]

- On Hype Cycles: "It is critical to separate the underlying platform shift of AI from the immediate, transient noise of the venture hype cycle." — Source: [Invest Like the Best]

- On Incumbent Advantage: "In the AI era, existing software giants with massive proprietary datasets and locked-in distribution have a profound structural advantage." — Source: [Startup for Startup]

- On Early Stage vs Late Stage: "The risk profile of venture has bifurcated; early stage is pure discovery, while late stage is heavily quantitative execution." — Source: [Insight Partners]

- On Automation: "Software ate the world by digitizing records; AI will eat the world by actually performing the labor." — Source: [Invest Like the Best]

- On Adaptability: "Firms that rely on the playbooks of 2015 will be entirely obsolete in the AI-native software ecosystem of the future." — Source: [Insight Partners]

Part 8: The Global Tech Ecosystem

- On Israeli Founders: "Israeli entrepreneurs are the highest quality entrepreneurs in the world. Period. There is a rare combination of integrity, work ethic, wisdom, and diligence here." — Source: [VC Cafe]

- On Israel vs Silicon Valley: "I often view the Israeli tech ecosystem as an upgraded, more resilient version of Silicon Valley." — Source: [Globes]

- On European Software: "Europe has transformed from a secondary market into a primary engine for deep-tech and highly complex enterprise software." — Source: [Insight Partners]

- On Global Ambition: "The best founders today think globally from day one; they do not build solely for their domestic market." — Source: [Startup for Startup]

- On Distributed Teams: "The pandemic proved that world-class software can be built and scaled by entirely distributed teams across multiple time zones." — Source: [Invest Like the Best]

- On Emerging Markets: "We are increasingly seeing infrastructure software emerge from regions that previously only produced consumer applications." — Source: [Insight Partners]

- On Cross-Border M&A: "Software consolidation is no longer a localized phenomenon; companies must be prepared to integrate international acquisitions to maintain dominance." — Source: [Invest Like the Best]

- On Local Ecosystems: "Our feeling as investors is one of deep confidence in local Israeli entrepreneurs – a feeling that is almost absent anywhere else." — Source: [VC Cafe]

- On Market Expansion: "Moving into the US market is the ultimate crucible for an international startup; it requires a complete recalibration of their go-to-market engine." — Source: [Startup for Startup]

- On Global Sourcing: "To be a top-tier firm today, your sourcing machine must be natively global, not just a US team taking occasional trips abroad." — Source: [Insight Partners]