Lessons from Jim Coulter

Jim Coulter co-founded TPG and helped move private equity beyond simple buyouts toward a model centered on operational growth. He navigates industrial shifts by applying "uncommon wisdom" borrowed from evolutionary biology and his farm roots. This profile looks at how that logic built the multi-billion dollar Rise Fund and his focus on institutional impact.

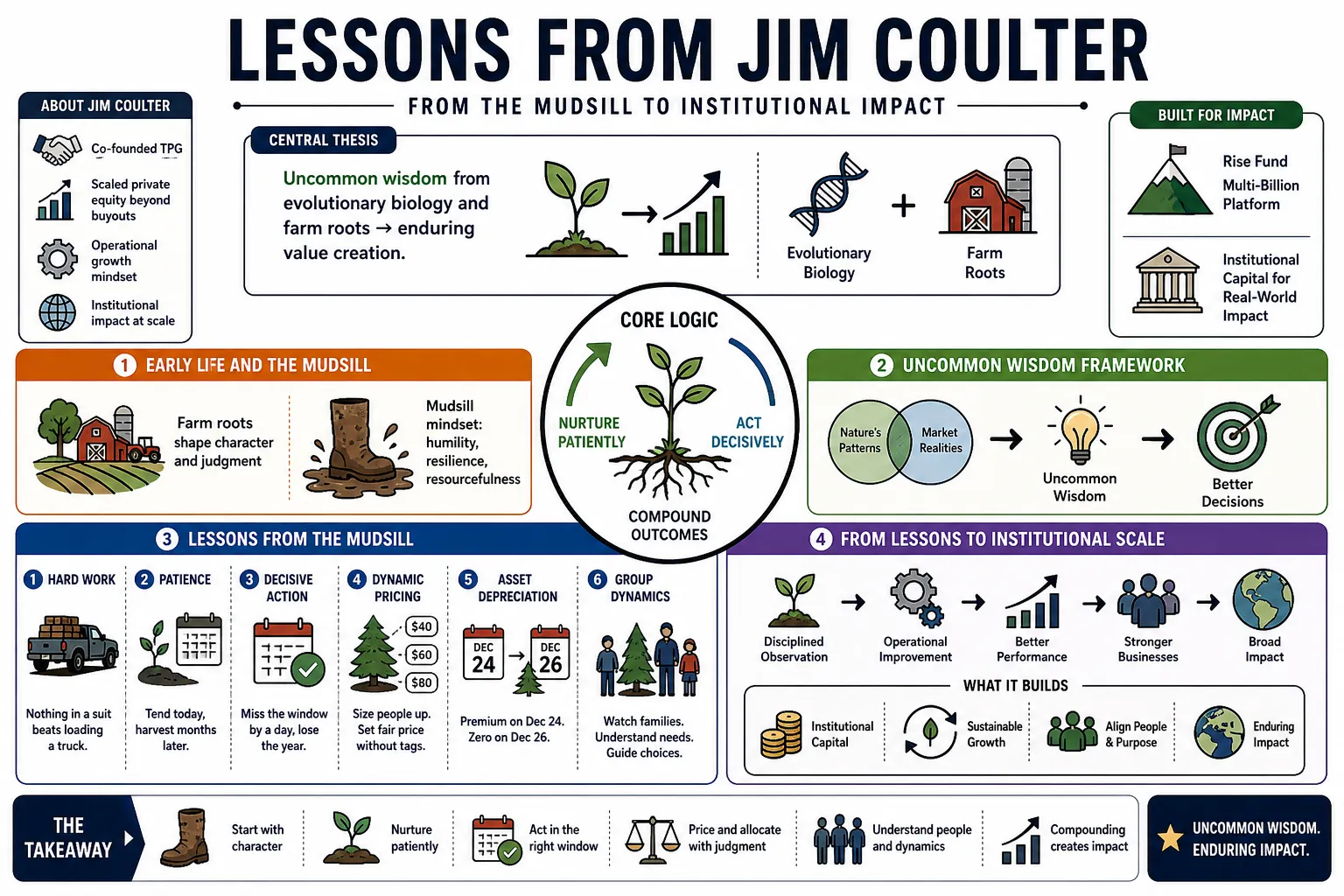

Part 1: Early Life and the Mudsill

- On Hard Work: "Nothing you can do to me in an air-conditioned building in a suit is going to be hard work compared to loading a truck on a farm." — Source: Stanford GSB

- On Patience: Farming requires the patience to tend a crop for months before seeing any tangible result. — Source: Stanford GSB

- On Decisive Action: Missing a harvest window by even a single day can result in the loss of an entire year’s work. — Source: Stanford GSB

- On Dynamic Pricing: Selling Christmas trees taught him to size people up on the lot to determine a fair market price without tags. — Source: Stanford GSB

- On Asset Depreciation: A Christmas tree is a premium asset on December 24th but holds zero value by the 26th. — Source: Stanford GSB

- On Group Dynamics: Watching families choose trees provided early insights into how groups reach consensus under pressure. — Source: Stanford GSB

- On Problem Solving: Farm life creates a mindset where everything is a practical problem that requires a hands-on fix. — Source: Stanford GSB

- On Negotiation: Negotiation is about reading the person across from you and understanding their specific needs in that moment. — Source: Stanford GSB

- On Foundations: The "mudsill" of success is built on the work ethic and practical wisdom gained in unglamorous settings. — Source: Stanford GSB

Part 2: The Continental Pivot and Early Deals

- On Continental Airlines: The hallmark of TPG was identifying "hairy" or complex turnarounds that others found un-investable. — Source: Alchetron

- On Independence: Believing in a transaction like Continental is worth more than the safety of staying within a family office. — Source: Alchetron

- On Marquee Transactions: A single successful, high-profile deal can establish a firm’s reputation for decades. — Source: Alchetron

- On the Great Man Risk: Over-reliance on a single visionary leader, like Mickey Drexler at J.Crew, can be dangerous when market tastes shift. — Source: Berkeley Law

- On the J.Crew Maneuver: Strategic legal moves to protect valuable intellectual property can become standard defensive tactics in distressed debt. — Source: Forbes

- On Burger King: Success often requires investing capital above the purchase price to fix the underlying infrastructure and franchisee health. — Source: Private Equity International

- On Operational Playbooks: There is a fundamental difference between building a brand through operational support and aggressive cost-cutting. — Source: Private Equity International

- On Neiman Marcus: Even "recession-proof" luxury brands are vulnerable to massive debt loads when the economic cycle turns. — Source: Berkeley Law

- On Strategic Optionality: Designing deal structures to preserve as many future paths as possible is a critical hedge in cyclical industries. — Source: Alchetron

Part 3: Investment Philosophy and Uncommon Wisdom

- On Uncommon Wisdom: "Investing is about uncommon wisdom... The most important thing I do is say no." — Source: Forbes

- On Punctuated Equilibrium: Industries often stay in stasis for long periods before hitting a "moment of mutation" that drives rapid change. — Source: Forbes

- On Stasis: You cannot generate outsized returns by investing in industries that are at rest; you must find the break. — Source: Forbes

- On Saying No: The discipline to reject 99% of deals is what allows you to commit fully to the 1% that matter. — Source: CNBC

- On Peripheral Vision: Success in a career requires looking at the edges of an industry where the next transformation is beginning. — Source: Stanford GSB

- On Cautious Courage: Investors should take measured, significant risks rather than following the safety of the consensus. — Source: Stanford GSB

- On Complexity: Complexity is not a deterrent but an opportunity for those willing to do the intellectual work to solve it. — Source: Bain & Company

- On the Rhythm of Crisis: Markets move through denial, planning, failure, and panic before reaching the "reality" stage. — Source: Forbes

- On Crisis Investing: The best time to underwrite a deal is when the market has finally reached the "reality" phase of a crisis. — Source: Forbes

- On Contrarianism: "When it feels bad, it's good" is a core tenet for finding value in distressed markets. — Source: Stanford GSB

Part 4: The Evolution of Private Equity

- On Leverage: "Leverage is a tool, but it’s like the hammer that sits in your toolbox. You don't use it as much when you have power tools." — Source: Bain & Company

- On Governance: Private equity has transitioned from a leverage business to a governance and growth business. — Source: Bain & Company

- On the Dead Sea Scrolls: 1989-style leverage-heavy deals are the "Dead Sea Scrolls of private equity," no longer relevant to modern returns. — Source: Bain & Company

- On Power Tools: Modern returns come from growth, changing margins, and fundamentally altering the business model. — Source: Bain & Company

- On Market Size: The public market is getting smaller and older, while the most interesting companies stay private longer. — Source: Bain & Company

- On Private Advantage: Younger companies thrive in private markets where they can focus on long-term transformation away from quarterly scrutiny. — Source: Bain & Company

- On Breaking the Tablets: Innovation in finance requires the willingness to question and break long-held industry conventions. — Source: Bain & Company

- On Institutionalization: A challenge for the modern industry is maintaining space for "unorthodox" figures who don't follow traditional paths. — Source: Bain & Company

- On Show, Don't Tell: Building a platform quietly allows the results to speak louder than any early promotional language. — Source: Tech.eu

Part 5: Climate and the Great Re-industrialization

- On Climate Scale: The world is about to undertake a $120 trillion re-industrialization to reach net-zero goals. — Source: Geekwire

- On the Digital Parallel: The current climate transition feels like the technology revolution in 1998; it will eventually touch everything. — Source: CNBC

- On Physical Revolution: Climate investing is a "physical revolution" that requires building real assets and infrastructure. — Source: Omny.fm

- On Greening Industrials: The goal is to rewire the entire industrial base of the country away from a carbon-heavy economy. — Source: Buyouts Insider

- On Capital Requirements: Governments cannot fund the transition alone; solutions must be driven by capitalist systems. — Source: Omny.fm

- On Climate Tourists: Investors cannot "pop in" and expect to succeed; climate is an immensely complicated revolution. — Source: YouTube

- On Assume Discontinuity: Expect industry "breaks" rather than linear progress as society moves toward decarbonization. — Source: YouTube

- On Bias to Action: "The path to progress and perfection starts with progress." — Source: YouTube

- On Transition Infrastructure: There is a massive opportunity in building the clean power backbone required for future energy needs. — Source: ImpactAlpha

- On Global Opportunity: While US policy is important, the climate transition is a global phenomenon with opportunities worldwide. — Source: ImpactAlpha

Part 6: Impact Investing and The Rise Fund

- On the Era of And: Investing can simultaneously deliver full market returns and significant social benefits. — Source: Tech.eu

- On Non-concessionary Returns: Impact investing must be unapologetically performance-based to be sustainable and scalable. — Source: Stanford GSB

- On Investing in Good: "It’s not just investing in good—it’s good investing." — Source: Tech.eu

- On Financial Blindness: From a purely financial point of view, an impact deal should look identical to any other high-quality deal. — Source: Stanford GSB

- On ESG Extra Credit: Impact investing goes beyond just avoiding harm (ESG) to actively solving global problems. — Source: Stanford GSB

- On Quantifying Impact: The use of the Impact Multiple of Money (IMM) allows firms to track social ROI with rigor. — Source: Stanford GSB

- On Building Platforms: TPG has scaled its impact platform to over $28 billion in AUM by proving the "Era of And." — Source: Milken Institute

- On Investor Bases: Nearly 75% of the investors in The Rise Fund come from outside the United States. — Source: ImpactAlpha

- On Solving Real Problems: Building companies that solve fundamental human needs is the most reliable way to generate real returns. — Source: Stanford GSB

- On the Relay Race: In the relay race of industrial change, the last leg is often the fastest. — Source: Geekwire

Part 7: Technology and AI

- On AI as Offense: AI is a transformative offensive weapon for private equity firms that act as change agents. — Source: Private Equity International

- On Defensive AI: The industry conversation is shifting from just protecting portfolios to using AI to drive growth. — Source: Private Equity International

- On AI Infrastructure: More power will be needed to fuel AI, opening up large opportunities in clean power generation. — Source: ImpactAlpha

- On Pause Investing: Providing capital to healthy companies during a temporary market "pause" allows them to maintain talent. — Source: Forbes

- On Technology 1998: The moment when society realizes a technology will touch everything is the most critical time to invest. — Source: CNBC

- On Clean Power: The "one thing that's clear" in the AI race is the massive increase in power demand. — Source: ImpactAlpha

- On Disruptive Models: Absorbing the innovative spirit of Silicon Valley helps a firm understand and lead disruption. — Source: Bain & Company

- On Industry Mutations: Successful investing requires catching moments of rapid mutation like the shift to digital streaming. — Source: Forbes

- On the AOL Phase: Many new industries, like climate tech, are currently in their "AOL phase" of early mass adoption. — Source: Omny.fm

Part 8: Leadership and the West Coast Offense

- On the West Coast Offense: A culture of precision, agility, and decentralized decision-making helps a firm stay ahead of Wall Street. — Source: Bain & Company

- On Short Passes: Focus on a high volume of precise strategic moves rather than just infrequent, massive buyouts. — Source: Bain & Company

- On Empowering the Quarterback: Deal leads should be empowered to think independently and call plays based on real-time market reads. — Source: Bain & Company

- On Preparation: Intense intellectual rigor and having a pre-determined thesis allow a firm to move faster when opportunity arises. — Source: Bain & Company

- On the Vital Unorthodox: Unconventional backgrounds are absolutely vital to the continued evolution of the investment industry. — Source: Bain & Company

- On the Talent Factory: The goal of leadership is to produce the next generation of investors who can run their own platforms. — Source: Bain & Company

- On Culture of Curiosity: Building a lasting firm requires a culture that encourages curiosity and constant learning. — Source: Bloomberg

- On David Bonderman's Legacy: The partnership with Bonderman was built on a shared commitment to thinking differently and embracing complexity. — Source: Bloomberg

- On the Important Lesson: The key question for any firm is whether the next generation of unorthodox pioneers would find a home there today. — Source: Bain & Company