Lessons from Josh Kopelman

Josh Kopelman founded Half.com before starting First Round Capital, where he helped shape the modern seed-stage venture model. He is best known for identifying the "Penny Gap," the steep psychological hurdle between a free product and one that costs a single cent, and for treating venture capital as a support platform rather than just a checkbook. This collection turns his track record into direct rules for surviving a company's earliest days.

Part 1: The Mental Models of Early-Stage Investing

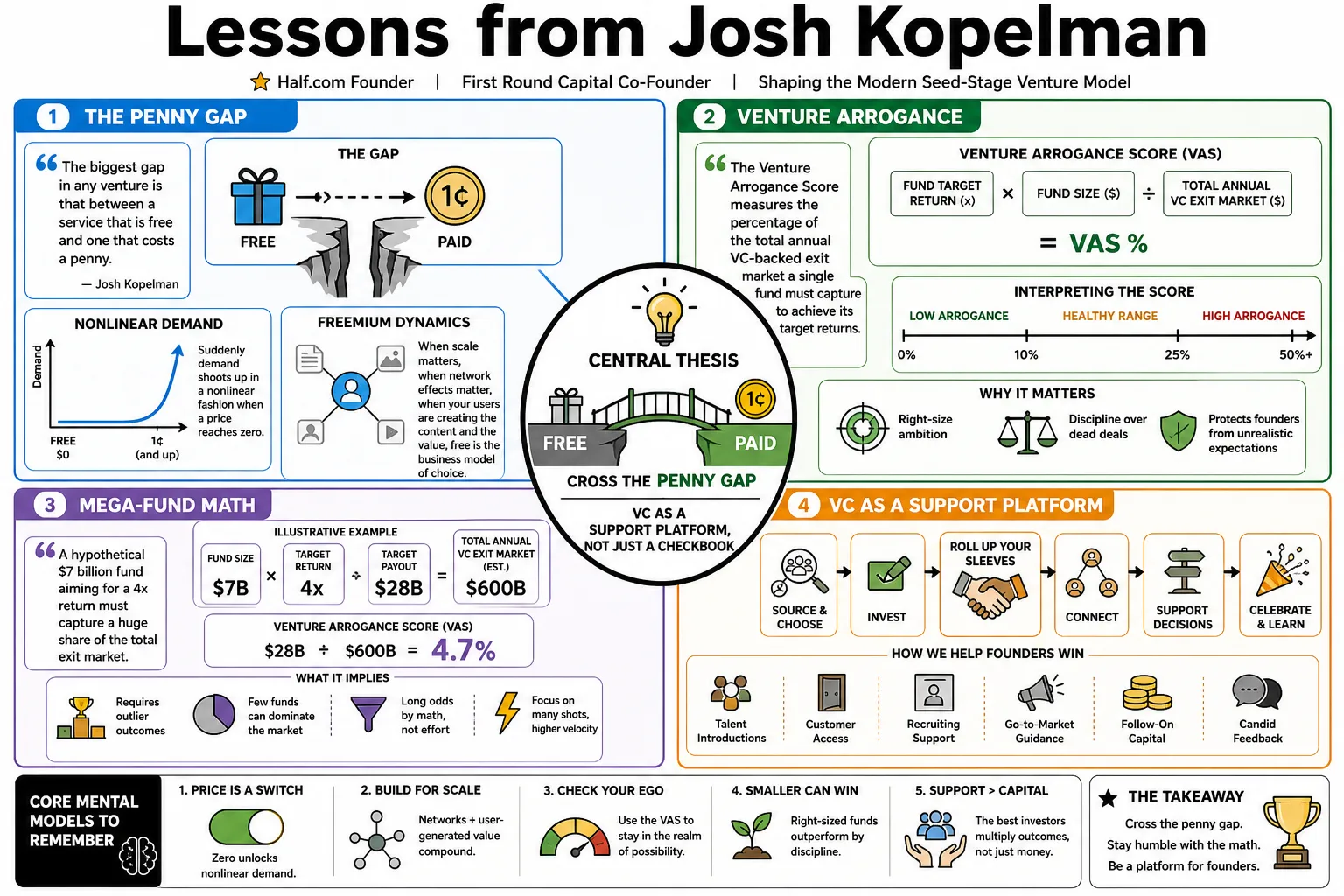

- On the Penny Gap: "The biggest gap in any venture is that between a service that is free and one that costs a penny." — Source: [First Round Review]

- On nonlinear demand: "Suddenly demand shoots up in a nonlinear fashion when a price reaches zero." — Source: [First Round Review]

- On freemium dynamics: "When scale matters, when network effects matter, when your users are creating the content and the value, free is the business model of choice." — Source: [AVC]

- On Venture Arrogance: "The Venture Arrogance Score measures the percentage of the total annual VC-backed exit market a single fund must capture to achieve its target returns." — Source: [Uncapped]

- On mega-fund math: "A hypothetical $7 billion fund aiming for a 4x return with 10% ownership would need to capture roughly 50% of all venture exit dollars annually—a feat never before achieved." — Source: [Invest Like the Best]

- On VC as jet fuel: "VCs sell jet fuel, which doesn't work in motorcycles. Bad stuff happens if VCs push jet fuel on a bike owner. Or if a bike owner thinks they can fly." — Source: [First Round Review]

- On the platform firm: "Most venture firms are a collection of features. We wanted to build a platform." — Source: [First Round Review]

- On exit alignment: "Founders might want a local exit like an early acquisition, while VCs need the express train to satisfy the power law of venture returns." — Source: [20VC]

- On returns in disequilibrium: "We don't make our money in equilibrium. Massive venture returns are generated during periods of irrational disequilibrium." — Source: [Invest Like the Best]

- On company math versus VC math: "There is a divergence between how founders and venture capitalists calculate success, particularly regarding exit valuations and fund returns." — Source: [Redeye VC]

Part 2: The Art of the Pick

- On the founder's most crucial choice: "A VC can pick dozens of companies, but a founder only has three or four 'picks' in their entire career. Each pick consumes five to ten years of your life." — Source: [First Round Review]

- On the time imbalance: "Most founders spend less than five to ten weeks picking an idea, but they're going to then spend five to ten years executing on that idea." — Source: [Sajith Pai]

- On set expansion: "The best pickers are people who are consistently focused on set expansion. They don't feel the time pressure of an arbitrary deadline." — Source: [Medium]

- On navigators versus cartographers: "Most of the best entrepreneurs are cartographers who create their own map versus navigators of existing maps." — Source: [Venture Almanac]

- On solving existing needs: "I don't like to solve new needs, I like to solve existing needs." — Source: [UPenn]

- On market size: "Markets really matter. Because the bigger the market, the more targets there are for the missile to hit." — Source: [QuoteFancy]

- On founder-market fit: "If you start a business in a space you don't know, you are spending your investors' money to get educated." — Source: [AlleyWatch]

- On the ease of pivoting: "It is much easier to change a solution than to change the underlying problem you are solving." — Source: [AlleyWatch]

- On the 'why now' question: "If I could give you the number one position on Google Search, what would it be? And is that a search people are searching for today or are you predicting they will search for it in the future?" — Source: [First Round Review]

Part 3: Finding Product-Market Fit

- On the 24-month hunt: "In all of the companies I started, my favorite time was the first 18 to 24 months. So much gets baked during that time. It's the hunt for product-market fit." — Source: [Substack]

- On the early-stage objective: "A startup's job is to learn, and a company's job is to grow. At the seed stage, your goal is to maximize learning per dollar spent." — Source: [First Round Review]

- On the 'imagine if' stage: "The earliest stage of a startup is the 'Imagine If' stage, where the goal is to de-risk the opportunity by proving the team can execute and attract customers." — Source: [Invest Like the Best]

- On optimization: "If you really want to be more like a startup, you must optimize for Product/Market Fit... the only thing that matters is Product/Market Fit." — Source: [Medium]

- On defining PMF maturity: "Product-Market Fit is not binary. It moves across four levels: Nascent, Developing, Strong, and Extreme." — Source: [First Round Review]

- On the burn rule: "Keep your burn rate as low as possible until you hit PMF. Nothing increases your odds of a successful Series A like customers who really love what you've built." — Source: [25iq]

- On compressed commoditization: "The time between an innovative feature and a widely available alternative is shrinking from years to months or even weeks." — Source: [First Round Review]

- On features versus systems of record: "If your startup is just a feature, it will be quickly commoditized by larger platforms. To survive, a company must evolve into a system of record that creates a sustainable moat." — Source: [First Round Review]

- On platform strategy: "Trying to build a platform from day one is extremely difficult. Platforms are a great way to scale a business, but not a great way to start." — Source: [Venture Almanac]

Part 4: Founder Mindset & Psychology

- On the burden of leadership: "Starting a company is amazingly lonely. Go out and find a community of peers to help and support you." — Source: [First Round Review]

- On exceptionalism: "People aren’t average until age 35 and then become exceptional when they choose to be Founder and CEO. Look for a history of being extraordinary." — Source: [Venture Almanac]

- On intellectual honesty: "The best founders have a firm grasp on what they know and what they don't know." — Source: [First Round Review]

- On embracing failure: "If all of you are always succeeding, you're not being aggressive enough." — Source: [Billy Penn]

- On pattern breaking: "Look for pattern breakers and founders who think differently about the world, who have gotten off the conveyor belt." — Source: [Venture Almanac]

- On tracking ideas: "Keep a journal and write down three things that went well and three things that didn't each day to find your next idea." — Source: [Cub Club]

- On the Peter Pan phase: "The first 24 months is the 'Peter Pan' phase. If you get your culture, core team, pricing, and positioning wrong in the first two years, they are nearly impossible to fix later." — Source: [Substack]

- On austerity bias: "There is a cognitive bias toward delaying painful actions like layoffs. In a downturn, the 'risk of ruin' increases every day you don't reduce your burn." — Source: [First Round Review]

- On false bottoms: "Markets often drop, stabilize, and then drop again. Don't assume the first sign of stability means the crisis is over." — Source: [First Round Review]

- On the lost year mental model: "During a downturn, ask yourself: 'What if I assume this entire year is a lost year for growth? How does that change my runway and my job for this capital?'" — Source: [First Round Review]

Part 5: Fundraising & Valuation

- On the tactical mission: "Great fundraising processes are run tightly, like a tactical mission. Containing information is a huge advantage for founders." — Source: [First Round Review]

- On the danger of raising early: "There’s enormous risk in raising too early. Once a company has taken more than a handful of meetings, it can be viewed as a 'shopped deal.'" — Source: [First Round Review]

- On the valuation trap: "Never turn down a deal based on valuation. It’s a mental trap." — Source: [20VC]

- On the art of pricing: "Ninety percent of the time valuation is science, but the art is knowing the 10 percent where you totally need to cave on valuation." — Source: [Venture Almanac]

- On risk versus reward: "Valuation should be viewed as the size of the opportunity divided by the amount of risk." — Source: [20VC]

- On the Series A crunch: "While seed capital is plentiful, the bar for Series A remains incredibly high." — Source: [First Round Review]

- On milestone-driven processes: "Only start a Series A fundraising process after you’ve hit major milestones. Starting too early is very risky." — Source: [First Round Review]

- On post-seed runway: "You should target 18 to 24 months of runway post-Series Seed. The best time to raise follow-on capital is when you don't need it." — Source: [25iq]

- On the first check: "For seed funds, ownership must be established with the 'first check' rather than trying to buy in later." — Source: [20VC]

- On pitch decks: "The moment an entrepreneur hits 'save' or 'print' the plan is out of date." — Source: [Medium]

Part 6: Hiring & Building the Core Team

- On the CEO's core duties: "You need to do two things as an early-stage CEO: hire the best possible people, and make sure you don't run out of money." — Source: [25iq]

- On time allocation: "If a founder is not spending at least 50% of their time hiring, they are already on the road to failure." — Source: [First Round Review]

- On selling the mission: "Hiring is almost always a seller's market for talent. Founders must sell the 'why' and the 'mission' more than the compensation." — Source: [First Round Review]

- On reference checking rigor: "Reference checking should be obsessive. Ask: 'I most likely am going to hire them and I could use your advice about how to best coach them to perform at their best from day one.'" — Source: [First Round Review]

- On the impact of early hires: "The team you build is the company you build. The earliest hires define the culture and trajectory more than any other factor." — Source: [First Round Review]

- On decision hygiene: "Founders should make implicit biases explicit and treat hiring as a high-stakes bet that requires a rigorous process." — Source: [Annie Duke]

- On the game tape of hiring: "We advocate for making the implicit explicit using standardized rubrics to capture independent thinking and avoid groupthink." — Source: [Annie Duke]

- On early culture baking: "So much gets baked in the first 24 months. You're building your culture. You're hiring your core team." — Source: [Substack]

- On small team economics: "If a small team of two to four people cannot reach ramen profitability within 6 to 12 months, it may indicate a fundamental issue with the business model." — Source: [NUS]

Part 7: Board Dynamics & Governance

- On asking versus telling: "The best board member isn’t always the person who has all the right answers, it’s the person who asks the right questions." — Source: [Podwise]

- On the role of the investor: "Our job is to bring out the best in the founder, not replace the founder’s insights with our own." — Source: [Deciphr AI]

- On the no surprises rule: "There should be a continual stream of information between meetings so that the board is never surprised by bad news during the actual session." — Source: [This is Going to Be Big]

- On delivering bad news: "If there is bad news, it should be shared with board members before the meeting to allow them to arrive focused on solutions rather than reacting emotionally." — Source: [This is Going to Be Big]

- On the 90/10 focus: "Board meetings should be 90% forward-looking on strategy, and only 10% backward-looking on reporting." — Source: [This is Going to Be Big]

- On presenting data: "CEOs should provide interpretation and analysis of the numbers rather than just presenting raw data." — Source: [This is Going to Be Big]

- On the first board meeting: "First board meetings are screwy. Founders should prepare no materials for the very first meeting, using that time instead to collaboratively define what future agendas should look like." — Source: [This is Going to Be Big]

- On new board members: "New board members should listen more than they participate in their first two meetings to understand how the entrepreneur thinks before offering prescriptive advice." — Source: [Venture Almanac]

- On the blessing of a skinned knee: "Allow startups to face adversity early to build resilience. It's the startup equivalent of Wendy Mogel's parenting philosophy." — Source: [First Round Review]

Part 8: Go-To-Market & Pricing

- On the Ebazon vision: "Solve an urgent and pervasive need but do it in a different way. Half.com succeeded by providing the fixed-price convenience of Amazon for the peer-to-peer marketplace of eBay." — Source: [Substack]

- On the TechCrunch bump: "A spike in traffic from a major press mention is not a sustainable marketing strategy and should not be mistaken for true product-market fit." — Source: [Startup Marketing]

- On the Stephen King pitch: "Avoid industry-speak. Asking 'How many of you have read a Stephen King book twice?' was far more effective than pitching a person-to-person marketplace for used mass media." — Source: [Substack]

- On the importance of customer data: "Borders had more daily foot traffic than Amazon had web traffic, but Borders was failing because they had no idea who their customers were." — Source: [Substack]

- On standing out: "In a crowded market, you need a hook that tells a story. Renaming a town 'Half.com' earned massive national coverage for a fraction of the cost of a traditional ad campaign." — Source: [Substack]

- On founder-led sales: "Founders who lean into sales and get good at selling will have a key advantage." — Source: [First Round Review]

- On the first customer: "The story of closing the first customer is a defining moment for a startup, as it represents the first true validation of the founder's narrative." — Source: [First Round Review]

- On the CEO as storyteller: "The CEO must be on the front line, constantly selling to customers, investors, and recruits, using a compelling story to bridge the gap between vision and a viable business." — Source: [a16z]

- On the difficulty of the first dollar: "The truth is, scaling from $5 to $50 million is not the toughest part of a new venture—it's getting your users to pay you anything at all." — Source: [First Round Review]