Lessons from Orlando Bravo

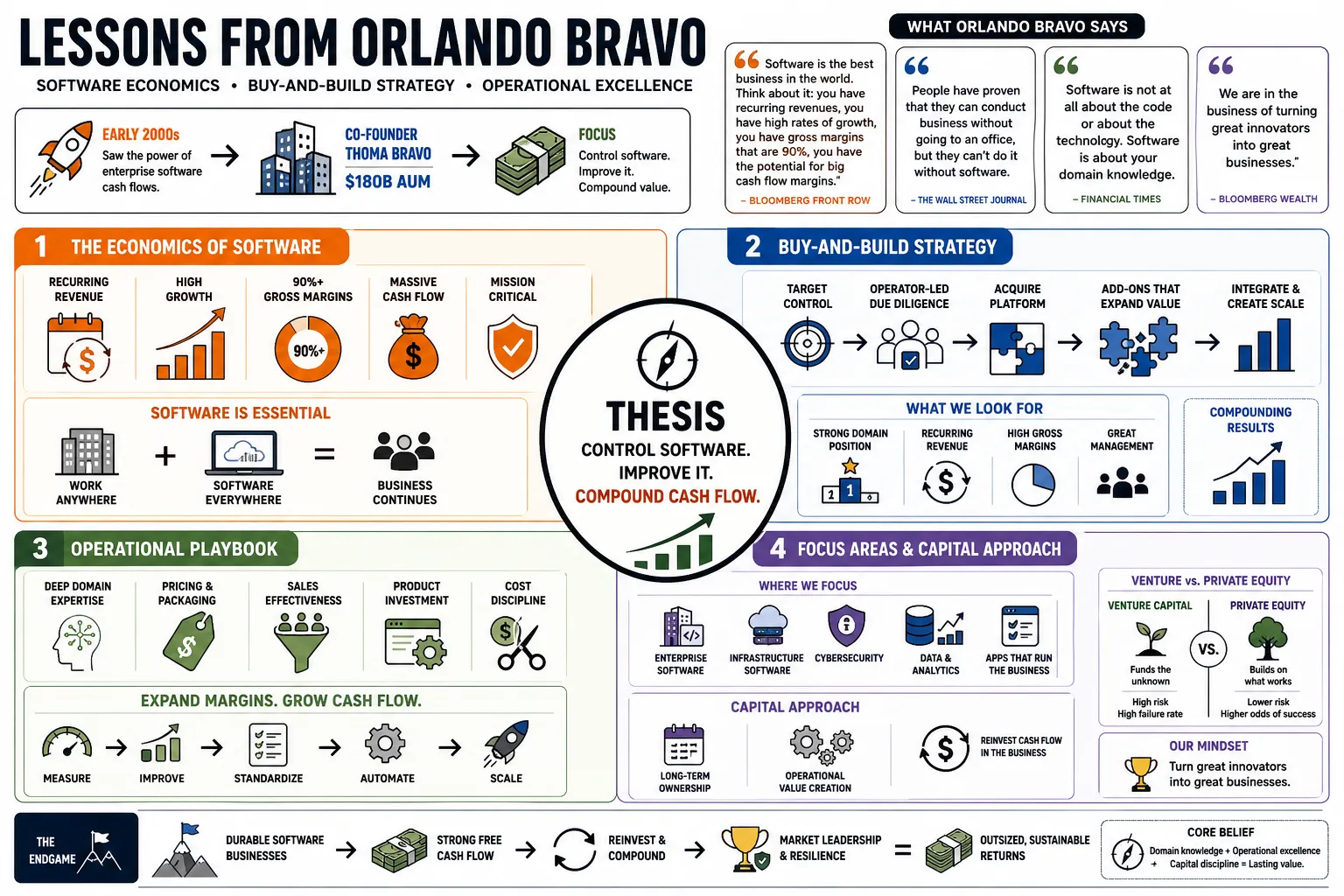

Orlando Bravo is the co-founder of Thoma Bravo, a $180 billion private equity firm built on his early-2000s realization that enterprise software could generate massive cash flow. This profile covers his approach to software economics, the buy-and-build acquisition strategy, and his operational playbook for expanding tech company margins.

Part 1: The Economics of Software

- On the best business model: "Software is the best business in the world. Think about it: you have recurring revenues, you have high rates of growth, you have gross margins that are 90%, you have the potential for big cash flow margins." — Source: Bloomberg Front Row

- On the necessity of software: "People have proven that they can conduct business without going to an office, but they can't do it without software." — Source: The Wall Street Journal

- On what really matters in code: "Software is not at all about the code or about the technology. Software is about your domain knowledge." — Source: Financial Times

- On industry focus: "We are in the business of turning great innovators into great businesses." — Source: Bloomberg Wealth

- On established software vs. startups: Venture capital funds the creation of software, but private equity is designed to take an established, mission-critical product and optimize its unit economics. — Source: Invest Like the Best

- On recurring revenue: Enterprise software companies are incredibly resilient because businesses simply cannot afford to stop paying for their core operating systems, even during a recession. — Source: Thoma Bravo Insights

- On economic dependence: "Software is everything. It is the business. It's what makes the business go." — Source: The Wall Street Journal

- On market moats: "Moats were always overstated... you have to always be producing the best product and taking care of that customer in an excellent way." — Source: CNBC Sohn Conference

- On switching costs: A software product's true value is measured by its gross and net retention rates; high retention proves that the workflow is sticky and switching costs are high. — Source: Invest Like the Best

- On the early days of tech PE: In the early 2000s, traditional private equity viewed software as too fast-moving and risky, creating a massive mismatch between capital and the quality of recurring-revenue businesses. — Source: Invest Like the Best

Part 2: The Buy-and-Build Playbook

- On the core PE formula: "Get the money, get the deal, improve the deal." — Source: Private Markets Insights

- On platform consolidation: The buy-and-build strategy relies on acquiring a market-leading platform company and then rapidly absorbing smaller competitors to expand the product suite. — Source: PE Hub

- On avoiding permanent holds: "The industry for a while there lost its way... people forgot to sell. Our industry is: you get the money, you try to transform a company as best you can, and then you sell that company." — Source: Bloomberg Talks

- On making buyers money: "The firm builds strong relationships with potential buyers by selling them companies that they make a lot of money from." — Source: The Wall Street Journal

- On the fundamental objective: You have to buy a specific company, not an index, and focus entirely on making that single entity structurally better. — Source: SuperReturn International

- On pricing power: Many software companies historically underpriced their products; enforcing pricing consistency and annual price escalators is a primary method for value creation. — Source: Invest Like the Best

- On taking a step back: "In order to realign the business and set it up for big-time growth, you first need to take a step back before you take a step forward. It's like boxing." — Source: Forbes

- On limiting team size: "If you have too big of a team, you become internally focused... the deal’s not in the office, the company’s not in the office, and the buyer of your company is not in the office." — Source: Bloomberg House Miami

- On the purpose of add-ons: Acquiring smaller rivals should be about fundamentally improving the domain capabilities of the core platform, rather than just adding revenue. — Source: Thoma Bravo Insights

- On deal velocity: The buy-and-build playbook is most effective when executed with speed, preventing acquired teams from languishing in integration limbo. — Source: PE Insights

Part 3: Margin Expansion and Profitability

- On the relationship between growth and margins: "We believe—and I feel we have proven this—that the more profitable you are, the faster you will grow." — Source: Bloomberg Front Row

- On the shift in valuation: Software companies can no longer trade purely on revenue multiples; a business is ultimately worth its future cash flows. — Source: PitchBook

- On setting margin targets: The goal for an acquired software company is often a hard reset to achieve 40% to 60% EBITDA margins while maintaining a double-digit growth rate. — Source: Invest Like the Best

- On R&D efficiency: Redirecting R&D to core features frequently allows firms to drop R&D spend as a percentage of revenue while delivering better products. — Source: PitchBook

- On sales and marketing spend: Cutting inefficient sales and marketing spend by analyzing true customer acquisition costs is a faster route to profitability than artificially inflating top-line sales. — Source: Forbes

- On operational metrics: Evaluating a company based on rigorous unit economics like EBITDA, free cash flow, and net income provides a much clearer picture of health than public market hype. — Source: CNBC

- On the Rule of 40: When applying the Rule of 40 to enterprise software, the weighting should heavily favor free cash flow margin over top-line revenue growth. — Source: SaaStr

- On eliminating bad practices: The remote work era introduced many bad managerial practices in software, requiring a renewed focus on operational stability to hit underwritten numbers. — Source: CNBC Money Movers

- On stock-based compensation: Real value creation requires fixing operations—such as managing geography costs and limiting excessive stock-based compensation—rather than relying on debt. — Source: Thoma Bravo Insights

- On operational alignment: Margin expansion is not a financial engineering trick; it requires rolling up your sleeves and aligning the management team with strict cash-flow objectives. — Source: The Wall Street Journal

Part 4: Evaluating Management and Leadership

- On CEO importance: "If the leader is good, everything is good. If the leader is not good, nothing is good." — Source: Private Markets Insights

- On listening: "I never created anything new. I just listened well. That’s a superpower." — Source: Stanford GSB

- On communication: "Focus on being a phenomenal communicator. Invest in that... why would somebody sell you that billion-dollar software company? That takes years of relationship and effort." — Source: Bloomberg Wealth

- On retaining existing talent: Thoma Bravo prefers to work with existing management teams rather than replacing them, provided the leaders adopt the firm's data-driven operational rigor. — Source: Invest Like the Best

- On the portfolio review process: Effective management evaluation requires intense, structured portfolio meetings that dive deeply into the unit economics of each business. — Source: Invest Like the Best

- On human judgment: "With AI, you can automate human judgment. And remember: AI is run by software, and AI is managed by software." — Source: CNBC Sohn Conference

- On taking responsibility for mistakes: "Medallia is a fine company... We made a mistake and that caused us to pay too much." — Source: The Wall Street Journal

- On avoiding the sunk cost fallacy: If a company does not perform well under the operational playbook, it is better to walk away than to endlessly funnel capital into a broken thesis. — Source: Bloomberg House Miami

- On founder relationships: Gaining the trust of a software founder requires understanding their product's domain deeply and proving that your operational changes will protect the company's legacy. — Source: Forbes

Part 5: Navigating Market Cycles and Valuation

- On market timing: "Private equity is not about market timing. As we say, we never buy the index. We never sell the index." — Source: SuperReturn International

- On capital deployment during downturns: Market corrections in software valuations create massive buying opportunities because public markets often overreact to macroeconomic fears. — Source: Financial Times

- On distinguishing true value: While some software companies deserve valuation cuts due to disruption, phenomenal businesses are frequently punished alongside them, creating arbitrary discounts. — Source: Thoma Bravo Insights

- On exiting large positions: Even when public market exits for large-cap tech companies are difficult, growing underlying earnings ensures that buyers will eventually emerge. — Source: CNBC Sohn Conference

- On standardizing returns: Returning cash to investors consistently, even in tepid environments, is the only way to justify raising massive subsequent funds. — Source: CNBC Squawk Box

- On public vs. private markets: Public markets price software companies based on narrative and momentum; private markets allow investors to price them based on controllable operational levers. — Source: Bloomberg Talks

- On the FOMO cycle: "The FOMO of being in any AI deal as early as you can in the private markets is pretty remarkable." — Source: The Wall Street Journal

- On managing portfolio perceptions: "What investors see for the most part is our companies are crushing it." — Source: The Wall Street Journal

- On simple investing advice: "Just buy the index. You don’t have to make this your full-time job... you’re going to be okay." — Source: Bloomberg Wealth

Part 6: Artificial Intelligence and the Future

- On AI disruption vs. enhancement: The companies that will thrive are those that use AI to enhance their deep domain expertise, not those easily replicated by generalized models. — Source: Bloomberg House Miami

- On the timeline of AI adoption: AI adoption in the corporate world will be an evolution rather than a revolution, likely taking five to ten years to fully transform operations. — Source: CNBC Davos Interview

- On building software from scratch: "Companies like OpenAI trying to build business software face the same challenge as every tech giant before them: creating entire business systems from scratch." — Source: The Wall Street Journal

- On the agentic era: "Our companies are incredibly positioned to be winners in the agentic era. Our companies are well on their way toward becoming AI-centric companies." — Source: Bloomberg Interviews

- On developer productivity: AI tools drastically reduce coding time, allowing companies to produce more features for the same cost base, which acts as a major tailwind for margins. — Source: SaaStr

- On the scale of the opportunity: AI represents a multi-decade growth opportunity for enterprise software, with an impact that will likely dwarf the transition to the cloud. — Source: CNBC

- On cybersecurity evolution: As data becomes decentralized in the Web3 and AI eras, cybersecurity must move away from simple perimeter defense to sophisticated, identity-based security protocols. — Source: Invest Like the Best

- On AI consolidation: Large incumbent software vendors are well-positioned to consolidate the market by acquiring smaller, specialized AI startups to broaden their platforms. — Source: CNBC Squawk on the Street

- On the limits of AI: Despite its power, AI cannot instantly replace the ingrained workflows, compliance adherence, and trust that legacy enterprise systems have built with their customers. — Source: Financial Times

Part 7: Philanthropy and Opportunity

- On the role of local circumstances: "It reminded me how local circumstances and access to opportunity play such a pivotal role in one's ability to succeed." — Source: The Wall Street Journal

- On bringing Silicon Valley to Puerto Rico: The Bravo Family Foundation aims to transfer the operational knowledge and business systems of private equity to local Puerto Rican founders. — Source: Bravo Family Foundation

- On disaster relief: Following Hurricane Maria, providing capital was secondary to establishing reliable supply chains that could physically deliver food and water to isolated communities. — Source: PR Newswire

- On startup acceleration: The Rising Entrepreneurs Program provides seed grants and mentorship to ensure young founders in Puerto Rico have the same baseline opportunities as those on the mainland. — Source: Thoma Bravo Philanthropy

- On empowering youth: Fostering an entrepreneurial mindset in high school and university students is critical to shifting an economy from dependence to innovation. — Source: Bravo Family Foundation

- On social enterprises: Nonprofits must be equipped with sustainable, revenue-generating models so they can serve underserved communities without relying solely on continuous donations. — Source: Bravo Family Foundation

- On equity investment: Philanthropy eventually scales into direct equity investment, helping established regional companies reach global markets through the Bravo Venture Fellowship. — Source: Bravo Family Foundation

- On operational knowledge transfer: Funding alone does not create businesses; founders need access to the rigorous metrics, scaling strategies, and network access utilized by top-tier investment firms. — Source: Bravo Family Foundation

- On closing the access gap: The ultimate goal of strategic philanthropy is to build a self-sustaining ecosystem where talent is matched with capital, regardless of geography. — Source: Bravo Family Foundation

Part 8: Personal Resilience and Advice

- On finding your path: "Find the risks that are meant for you to take." — Source: Stanford GSB

- On learning from failures: "You can make mistakes, but don’t make similar mistakes." — Source: Stanford GSB

- On focus: "Do the work, focus on your business, focus on you, and do your thing. That will pay huge, huge dividends." — Source: Stanford GSB

- On dealing with impostor syndrome: "I thought you know I had to work so hard... and I'm like now that I made it into private equity, I'm going to get fired." — Source: The Wall Street Journal

- On starting over: "You could be the number one seed at a tournament... and the next one you have to win the first round against a really tough opponent. You start from zero every time." — Source: SuperReturn International

- On competitive endurance: "It’s okay not to always be the best at everything... you just try your hardest and you do your own thing." — Source: Stanford GSB

- On second chances: The trajectory of a career often depends on the grace of a mentor who is willing to give you a second chance after an early, high-profile failure. — Source: Invest Like the Best

- On ignoring the crowd: By focusing on unglamorous software buyouts when everyone else was chasing consumer internet startups, he proved the value of ignoring consensus. — Source: Invest Like the Best

- On maintaining perspective: True success requires looking past the immediate noise of the market and committing to the foundational metrics that actually dictate business health over decades. — Source: Bloomberg Wealth