Pierre Lamond helped build the early semiconductor industry as an executive at Fairchild and National Semiconductor before his three-decade run as a partner at Sequoia Capital. He was a notoriously practical investor who demanded that founders know their technology cold, keep costs down, and go after huge markets. This profile covers his core rules for operating and investing, drawn from a career spanning the first integrated circuits to modern industrial hardware.

Part 1: The Foundations of Innovation

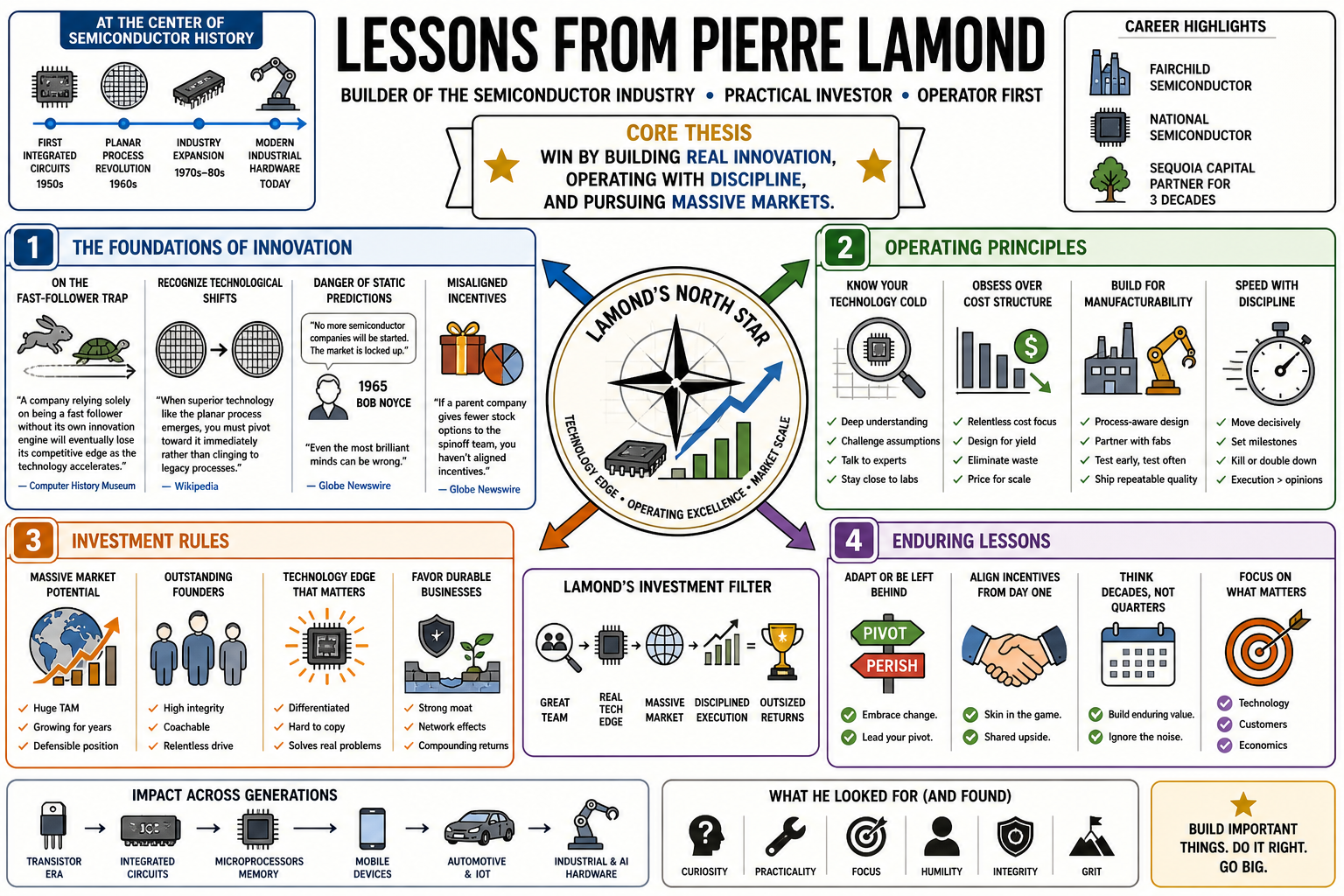

- On the fast-follower trap: "A company relying solely on being a fast follower without its own innovation engine will eventually lose its competitive edge as the technology accelerates." — Computer History Museum

- On recognizing technological shifts: "When superior technology like the planar process emerges, you must pivot toward it immediately rather than clinging to legacy processes." — Wikipedia

- On the danger of static predictions: "Even the most brilliant minds can be wrong; in 1965, Bob Noyce predicted no more semiconductor companies would be started because the market was locked up." — Globe Newswire

- On misaligned incentives: "If a parent company gives fewer stock options to the profitable divisions than the unprofitable ones, the top talent will leave and start your competitors." — Computer History Museum

- On capital focus: "Corporate parent companies fail when they use core business profits to fund unrelated, unprofitable ventures instead of reinvesting in the winning technology." — Computer History Museum

- On technical fundamentals: "I was one of the few engineers that knew something about electronics and knew also about how transistors really work because I had read that book and studied it." — Computer History Museum

- On corporate politics: "Do not tolerate manufacturing incompetence; if your direct supervisor cannot hit production volume, bypass them to fix the bottleneck." — Wikipedia

- On financial engineering: "Building a company merely to drive high profit margins for a quick IPO valuation starves the research engine needed for long-term survival." — Computer History Museum

- On early brashness: "If you don't raise me to $6,000, I'm going back to France." — Computer History Museum

Part 2: Operational Rigor and Manufacturing

- On process engineering: "Instead of constantly inventing new manufacturing methods, standardize and improve your existing ones to maximize yield." — Globe Newswire

- On cost leadership: "Moving assembly to offshore hubs is a necessary strategic step to drastically reduce costs and remain competitive." — Wikipedia

- On market transitions: "Shifting focus from low-volume military contracts to high-volume commercial markets is the path to scaling an electronics business." — Wikipedia

- On frugality: "Operating a lean, frugal company is a direct and necessary reaction to the corporate waste that kills early technology leads." — Globe Newswire

- On operational excellence: "While research and development form the heart of a company, operational discipline and manufacturing efficiency are the lungs." — Globe Newswire

- On evaluating talent: "Dave Widlar is probably the best engineer I ever worked with. He was unbelievable, very inventive, extremely thorough, leaving no stone unturned." — Computer History Museum

- On the execution gap: "Great technology routinely fails without a great supply chain and rigorous cost control backing it up." — Globe Newswire

- On the limits of invention: "Innovation gets you to the starting line, but relentless yield optimization is what actually builds the business." — Wikipedia

- On operational transparency: "Do not hide manufacturing flaws behind marketing; fix the physical production line first." — Computer History Museum

- On the "tight ship": "Run the tightest ship possible, standardizing every variable you can control so you can weather the variables you cannot." — Wikipedia

Part 3: The Craft of Venture Capital

- On the essence of VC: "A focus on growing companies from scratch is what venture capital is all about, not just because this is exciting, but it is also the way to make money." — VentureBeat

- On entry timing: "Typically our style of investment is to invest early. First, we try to identify potentially profitable sectors of the market before everyone else does." — Wikipedia

- On taking responsibility: "At that point, we get involved in the seed and first financing rounds, become active at the board level, establish strategy, and recruit a management team." — Wikipedia

- On spotting hype: "We're in a Web 2.0 bubble in my opinion." — Wikipedia

- On passive financing: "Writing a check is the least important part of venture capital; building the management team is where the actual return is generated." — VentureBeat

- On venture as a trade: "Venture capital is an apprenticeship business where the gut feel for evaluating founders is passed down through direct observation." — Medium

- On professional relationships: "It is not to your advantage to have an uncivil relationship with your former partners; leave clean and keep your equity interests aligned." — Wikipedia

- On operator experience: "An investor who has run a factory floor brings a different level of scrutiny to a startup than someone who has only studied finance." — VentureBeat

- On identifying capability: "The primary task of an early-stage investor is identifying true technical talent versus individuals who are simply good at selling." — VentureBeat

- On company building: "Venture capital is not momentum investing; it is the fundamental construction of new economic engines." — Full Ratchet

Part 4: Sizing and Market Dynamics

- On absolute scale: "I understand why you like it, but it cannot be that big. If it isn't that big, it won't make a great venture return." — Full Ratchet

- On the cause of death: "Companies are not failing on technology, they will always fail on the market." — Full Ratchet

- On the ultimate metric: "Revenue solves all problems; it covers up hiring mistakes, technical debt, and morale issues." — SuperScout

- On acquisitions: "Companies are not getting sold, companies are getting bought. Build something acquirers actually need." — Full Ratchet

- On interesting ideas: "If a startup addresses a niche that mathematically cannot scale to an industry-defining size, pass on it regardless of how elegant the solution is." — Full Ratchet

- On the physics of products: "Investors must understand the underlying physics and unit economics of a product before assuming the market will accept its price point." — Computer History Museum

- On features versus businesses: "Many founders mistake a clever software feature for a standalone business; if the market size is small, it belongs inside another product." — Full Ratchet

- On momentum investing: "Investing based on what is currently popular guarantees you are entering the market too late and paying too much." — SuperScout

- On market validation: "Do not fund companies trying to educate a market that does not want to learn; fund companies serving an obvious, quantified hunger." — Full Ratchet

Part 5: Board Leadership and Founder Mentorship

- On board accountability: "Ask 'How is your traffic coming along?' at every single meeting; founders must know the core metric is being watched relentlessly." — VentureBeat

- On technical scaling: "When user adoption outpaces infrastructure, the only mandate for the board and the founder is 'More bandwidth.'" — VentureBeat

- On founder autonomy: "You cannot enforce the founder. If the founder wants to sell, you let them sell because at the end of the day, he ran the company." — Full Ratchet

- On the shadow board: "Experienced partners should shadow junior partners on high-growth boards to provide seasoned negotiation experience during unexpected scaling events." — Wikipedia

- On the reality of hypergrowth: "Exponential growth is messy, expensive, and stressful; the board must manage this reality rather than demanding immediate, tidy profitability." — VentureBeat

- On working styles: "A successful board adapts to the culture of the founders, even if it means holding meetings in an empty office while the engineering team sleeps." — VentureBeat

- On keeping the edge: "A stern demeanor in the boardroom prevents founders from becoming complacent and keeps them focused on month-over-month progress." — VentureBeat

- On exit strategy: "Guide founders toward a strategic exit when capital requirements to sustain infrastructure outpace their ability to raise non-dilutive funding." — VentureBeat

- On tough questions: "The board is there to ask the hard questions that transform a long-shot project into a structured, global business." — VentureBeat

Part 6: Deep Tech and Scientific Boldness

- On returning to deep tech: "Joining a firm focused on bold, scientific companies is a return to the source of what venture capital was meant to fund." — Wikipedia

- On hard problems: "Venture capital should target difficult sectors like energy storage and water purification instead of defaulting to consumer software." — Wikipedia

- On the limits of social apps: "There is a hard ceiling on the value created by social media trends compared to the value created by fundamental scientific breakthroughs." — VentureBeat

- On evaluating science: "An investor must possess the technical literacy to distinguish between viable applied science and theoretical lab projects that cannot scale." — Computer History Museum

- On long development cycles: "Scientific companies require a different capital structure and a longer timeline than traditional software investments." — Wikipedia

- On hardware moats: "A company built on a genuine scientific advancement possesses a defensive moat that cannot be replicated by a competitor with a larger marketing budget." — Wikipedia

- On engineering rigor: "Apply the same standard of exhaustive, inventive engineering required in semiconductor design to modern clean-tech investments." — Computer History Museum

- On capital intensity: "Be prepared to fund heavy capital expenditures early if the underlying science dictates that physical infrastructure is the product." — Wikipedia

- On backing scientists: "The ideal technical founder has the deep domain expertise of an academic but the pragmatic urgency of an industrial engineer." — Computer History Museum

Part 7: Digitizing the Physical World

- On the industrial evolution: "The next massive economic opportunity lies in digitizing physical industries that have been neglected by software investors." — SuperScout

- On the full-stack approach: "Solving complex industrial problems requires integrating hardware, software, and data into a single, cohesive system." — SuperScout

- On venture equity: "If a market gap exists where a physical solution should be, use venture capital to build the company from scratch and hire the founding team yourself." — Full Ratchet

- On the hardware barrier: "Hardware is no longer the insurmountable barrier it once was, provided it is directed by an intelligent, software-driven architecture." — SuperScout

- On human augmentation: "Technology in physical environments should focus on augmenting human workers to boost productivity rather than attempting fragile, full automation." — SuperScout

- On the ten-year horizon: "Building in the physical world requires preparing founders for a ten-year journey defined by discipline, integrity, and humility." — SuperScout

- On de-risking atoms with bits: "Iterate rapidly on the software layer to offset and de-risk the slower, more expensive iterations required in hardware." — SuperScout

- On unglamorous markets: "Construction, logistics, manufacturing, and defense are the permanent bedrocks of the economy; invest in them over shiny consumer objects." — SuperScout

- On team dynamics: "The foundation of a hardware startup is a small, highly functional team operating with absolute, military-grade trust." — SuperScout

- On thesis-driven hunting: "Map entire physical markets to identify structural flaws, then actively hunt for the specific team capable of fixing them." — Full Ratchet

Part 8: Personal Philosophy and Resilience

- On surviving adversity: "I'm the proof that you can survive. No, it was a very difficult time in occupied France, and I survived." — VentureBeat

- On refusing to stop: "What retirement?" — Wikipedia

- On late-career balance: "I really have the best of both worlds. I can work as hard or as lightly as I want. Don't worry about me, I'm very comfortable." — VentureBeat

- On self-education: "Read the foundational texts of your industry and study them until you understand how the components actually work." — Computer History Museum

- On direct communication: "A lack of small talk is not a lack of respect; focusing entirely on data and progress is the highest form of professional respect." — VentureBeat

- On global talent: "When there is a lack of local engineering talent, you must recruit globally to ensure your company has the intellectual capital it needs." — Computer History Museum

- On demanding excellence: "If your superiors are making poor technical decisions, it is your obligation to speak up and prove you can run the operation better." — Wikipedia

- On longevity in business: "Endurance in technology investing comes from a constant willingness to abandon old models when a better physical reality presents itself." — Computer History Museum

- On remaining a student: "Never assume the market is settled; the moment you believe the big players have locked up the future is the moment you miss the next wave." — Globe Newswire